Are the days of ZIRP over for the Fed?

The market over-prices the chance of <1% rates, failing to take into account the changing psychology of the humans that run the Fed

In response to the debt overhang that encouraged the GFC, the Fed moved to ZIRP (zero interest rate policy) after Lehman Brothers collapsed. It maintained this position for 7 years until Janet Yellen hiked away from zero rates in 2015.

Utter panic was likely the primary driver given the situation that the financial system found itself in, but worry about outright deflation was something that had been building in the Fed for a number of years up until that point.

ZIRP has probably caused of a lot of issues. It has likely prompted over-investment of capital in a number of areas and resulted in a generation who see the Fed as an entity that has increased inequality and has done the most to make sure the status quo prevails.

Getting out of ZIRP has had its fair share of issues as well, and these problems required more assistance from the Fed at the same time it has been trying to reduce accommodation, offsetting it.

Has this timeline had a sufficient enough effect on the Fed so that it won’t want to go back and try do this again?

Firstly we need to look at how the market prices a possible journey back towards ZIRP.

Guessing the market’s probability

There is no perfect answer to determining the probability of a certain path of rates.

The forward yield curve describes the central expectation for future interest rates. It takes all of the factors that market participants are using to trade and describes an average outcome given those factors.

Some of these traders may be forecasting an actual realistic forward path for Fed Funds based on their forecast for growth and inflation, for example.

Alternatively, other traders may be looking at Fed Funds at the end of 2024 and saying to themselves, “there is some chance Fed Funds by that time will be 0.25%, so I’ll just buy”.

This trader might think the Fed will still be above 5% by then. However, since there is a non-zero chance of a crisis occurring, so they will accept paying a “premium” to hedge against this outcome. The “premium” is contained in the inverted curve.

The second trader might also be hedging a book of other assets that will suffer if the crisis scenario occurs. They are happy to accept a less than ideal return on these positions as long as an adverse outcome is avoided, in which they will gain nicely on the rest of their portfolio.

Normally, the effects of this type of “insurance buying” should net out in an efficient market, as forward expectations should be evenly distributed around the current level.

For interest rates this is rarely the case as the future path to rates can be asymmetric. If we want proof of this, we just need to look at the options market.

Using options to understand the market’s bias

Estimating probabilities for outcomes in the options market is easy – the “delta” of an option is just the probability that an option will be exercised, or end up “in the money” at expiry.

For deep out of the money options, the most important determinant of the delta is the implied volatility of that option. The higher the implied volatility of the underlying spot price of an option, the higher the chance a price will end up so far away as to get all the way past the strike price.

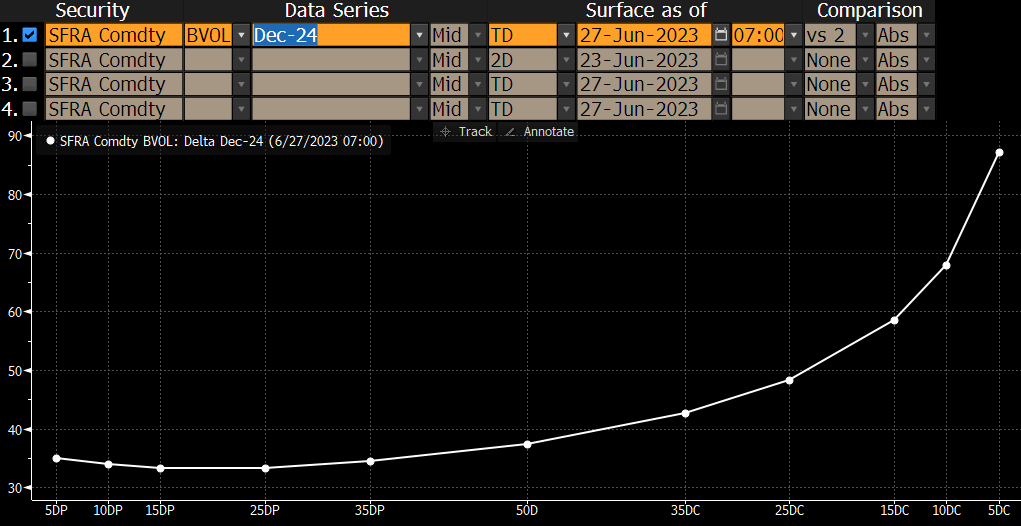

If you chart all of the implied volatilities for options against their delta, it paints a picture of which outcome the market is more worried about. Below is that chart for Dec-24 SOFR futures.

The “50D” point describes options that are “at the money”, which is at a 4% forward interest rate.

On the left, “10DP” describes the implied volatility for put options at 10 delta that are well out of the money. They are options you would buy if you think rates are going much higher than they are (to about 7%). These trade at about 35 (norm) vol.

On the right side we see the same but for options that will exercise if rates fall a lot. The “10DC” point describes options with a strike price around 2% lower than where the expectation is now (which is 4%). Here the implied volatility is at about 70 vol, double the value of the puts.

Since all of these options have the same underlying security, that being the Dec-24 SOFR future, the volatility estimated by the market should be the same no matter the strike. But it isn’t!

A skew in this volatility curve is present because the market values “rates down” protection much higher than “rates up” protection.

The shape of this curve tells us that tail risks are strongly one way, and therefore asymmetric.

The problems with the options market

When you look at the options market, you might think that the percentage chance that rates go to zero is still priced quite lightly.

If the probability on rates being less than 1% by the end of 2024 is only around 4%, then the chances it goes to zero are much less than that. This is true from a literal reading of the deltas traded by the market.

However, this probability is for the option market alone, and not for all market participants. As a result it doesn’t take into account how spot yields are affected by people buying the outright through futures and swaps as a method of portfolio protection.

How we determine where spot yields “should be” is the question, however.

A more flat to slightly inverted yield curve is a fairer expectation given it’s theoretical basis and persistence over history. However, the classic “this time is different” argument is in play this time, as low potential growth becomes the magnet for rates if inflation finally cools back down to 2%.

When it comes to which argument is more likely, I am firmly in the camp of considering the current level of rates to be correct until the inflation or growth data suggests otherwise.

If the forward path of rates is correct and the Fed is set to cut rates after 2023, this would represent unprecedented perfection in the timing and the magnitude of the Fed’s reaction to falling growth and inflation which hasn’t even happened yet.

The forecast errors involved are insurmountable, and lend themselves to an explanation for a steeply inverted curve that don’t require such outcomes that are “priced to perfection”.

An easier way to explain the sharp inversion in forward rate expectations is that the market is looking for at least a flat carry hedge against risky assets where a left-tail event in which Fed Funds will be cut to zero.

If Fed Funds ends up staying at their current level throughout 2024 and 2025, there will be mark-to market losses on these rates hedges. Towards maturity however these losses will reverse, and the total P&L of the positions will still be positive, representing the coupon earned over the period. These positions will underperform cash, but still produce a positive absolute return over the period.

Why would you bother buying deeply out-of-the-money options and attract certain cost to hedge a disaster outcome when bonds pay you to do it?

A flat to slightly inverted curve would take into account a proper normally distributed expectation after 2023. This would mean that any further inversion could be driven by buyers that seek portfolio protection based on the expectation that the Fed would cut to zero again in a financial crisis.

This would put another journey below 1% by end 2024 rates at around 25%1, far higher than the option market expected 4%. This deviation is fair given the relative cost to a portfolio of the two instruments.

Is 25% chance Fed Funds ends up below 1% over 18 months too high? I think so, and it is a solid argument for shorting the 2024-2025 part of the curve.

Why does the market ascribe such a large premium? The argument is more nuanced than it first appears, but it’s worth covering off the most obvious objection first.

Duh, of course they’ll cut to zero again

By far the most common response is “duh, of course they’ll cut to zero again” (also commonly prefaced with “you’re an idiot”).

The assertion is rarely expanded any further than this, but everybody knows why this is the default view. When you have an addict in a room with whatever they are addicted to, there is a pretty good chance they will eventually be convinced by it again.

Politics adds to this as well. It would be silly to think that the sitting president wouldn’t affect rates. Indeed, Donald Trump was very vocal on this issue, and it’s hard to see him changing his view if he is successful in 2024. If foreigners want to own US government debt so badly, then why pay them for the pleasure?

Fiscal policy may have taken over from monetary policy as the primary tool to smooth out the natural economic cycle, however we can’t discount the powerful messaging and sentiment effect fast cuts to the Fed Funds rate have.

Cutting interest rates can help restore confidence when the economic challenges involve threat to the very existence of the financial system, and this was the very argument in 2008.

In 2008, ZIRP didn’t save the system though. The equity market didn’t reach a low until March 2009, when Congress did something about actually backstopping toxic assets on bank balance sheets. Despite this, ZIRP is still considered an important pillar of the response to the failing banking system in 2008, and will likely remain as a tool if we ever faced anything as serious as this situation in the future.

Do the “of course they’ll cut to zero again” crowd still think zero rates will come about if we have a regular slowdown that doesn’t involve a financial crisis? The perma-bears will say yes, but there is no historical analogue for it, with most economic slowdowns being matched with more modest cuts to the Fed Funds rate.

It’s tough to remember however, as a normal slowdown hasn’t happened for 22 years, and that the last policy cycle we had (the pandemic) resulted in an immediate cut to zero again.

Ultimately the “of course they’ll go to zero again” brigade will be right if we faced another broad credit crisis like in 2008. It will need to be something large, as the Fed has a tighter control of the system than it did then.

Outside of that, I think that the conversation has shifted more towards the concerns around what extreme monetary policy has done, and that inflation is no longer impossible with the right conditions.

The one-way effects of fast tightening

They may not take responsibility for it publicly, but central banks will be cognisant of problems they have caused in many other parts of the financial system by hiking rates this quickly.

In the US, banks (and most notably small banks because of other disadvantages inherent in the structure of the system) suffered because of capital losses on their bond holdings. UK pension funds struggled with collateral obligations on the fast falling value of their long-term bond holdings.

Closer to home for CBs has been the destruction of net equity on central bank balance sheets from losses taken on bond holdings acquired at the absolute low in rates during the pandemic.

It isn’t the hiking cycle that should be blamed here, however. High inflation should elicit this reaction, given the known reaction function. Where the problem was caused was not in hiking, but in the cutting before that.

The speed and aggressiveness during 2022 wouldn’t have been required if rates weren’t so low in the first place. ZIRP was the problem, not the need to normalise.

The market is naturally long duration, receiving coupons as bond investors. While there will be a reinvestment issue in the future if rates fall a lot, most benefit from capital gains on their bond holdings now.

Those supplying bonds, the government and corporates who issue debt, are happy as well. There is no adverse “mark-to-market” for issuers, and as a bonus they can look forward to lower rates when they roll their debt in the future.

There are fewer winners when rates rise. Savers may benefit from better coupon rates in the future, but right now they have to nurse significant capital losses. Corporates and governments have to deal with a future where interest payments may be 3 times what they were before.

This isn’t to say that rates shouldn’t increase. It’s just that the magnitude of the increase really matters now. With so much financialization now when compared to the ‘70s, rate hikes just can’t be as fast and large as they were in the past. Things will break, and they have.

Inflation has ruined everything

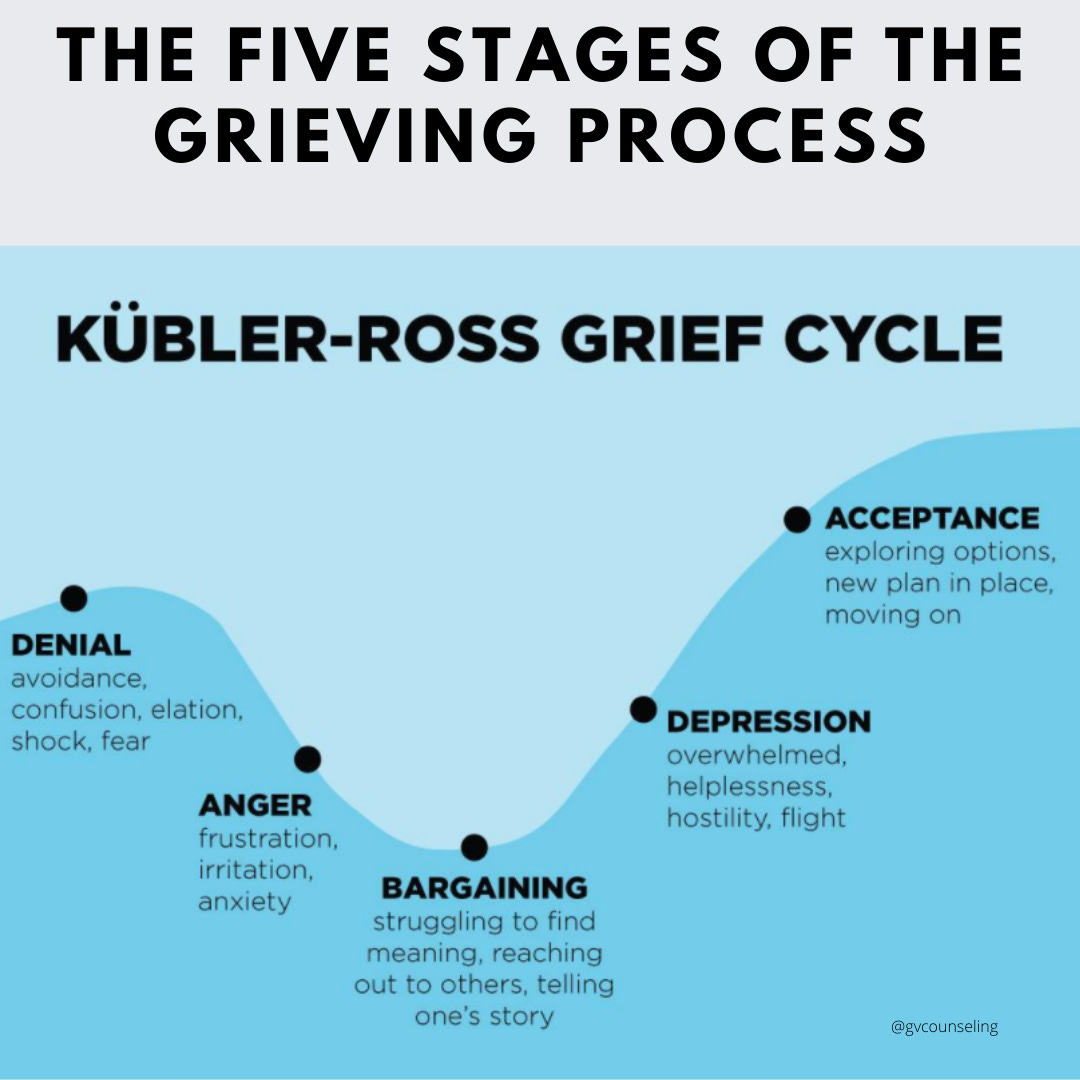

The Fed’s reaction to the return of inflation follows the Kubler-Ross grief cycle almost perfectly.

Denial and anger manifested themselves in the persistence with the “transitory inflation” rhetoric which dominated the early part of this inflationary episode. The market was similarly unwilling to accept that rates needed to rise substantially – a lot was invested in rates staying low.

The bargaining and then depression episodes were experienced in mid-2022, as central banks really struggled to map out a path to deal with inflation that clearly wasn’t “transitory” any more. The cadre of central bankers that not only spoke about unbounded upside to rate hikes while delivering 50-100bp per meeting, causing panic and severe volatility.

2023 saw the transition to “acceptance”, where central banks are more comfortable with the persistence of inflation and their approach to dealing with it. Rate hikes are more measured. As a result, rates market volatility is down substantially.

The reality of what comes with “acceptance” is that its permanent deflationary outlook will now have to change.

The psychology of the central banker

The 5 stages of grief are linked to monetary policy because central banks are run by humans, and while they try to constantly show that there is data behind their decision making, they still make qualitative decisions which are driven by how they will be viewed now and into the future.

This is exactly why central banker thinking about large macro concepts such as inflation and GDP growth tends to move in low-frequency waves. The next central banker will inherit the biases of the last, unless there is a horrific change in the market environment.

In this piece I track how the Fed very slowly changed their opinion on the risks to inflation over two decades. The fear of the ‘70s stuck around until the late ‘90s, where the dot-com bust and September 11 introduced a wholesale shift towards deflation as being more of a risk than runaway inflation.

This point in time represented a change to how central bankers thought about inflation in nearly 30 years. Ben Bernanke’s actions during the GFC by introducing ZIRP and QE are less significant than that shift over the turn of the century, even though the GFC itself was a more significant event. This psychological shift changed the structure of the market.

The longer that the current inflation episode persists, the stronger the experience of inflation will mould the psychology of bankers at the Fed, the ECB and others.

Never forget that economics is a social science

Economic theory is mostly untestable, and as such economics fails to qualify as a proper science. For this reason popular theory is subject to herd thinking.

For the last 20 years, the fast-to-cut mentality due to a fear of deflationary impulses taking hold has given a strong negative correlation of equities and bonds.

The success of this strategy in navigating the world out of the GFC gave subsequent bankers the confidence to continue with the same behaviour, driven by the same theory.

The one-sided and extreme approach to inflation risks (or in this case deflationary risks) put central banks all-in on low rates. Getting out of this situation created more problems than it would have otherwise if they took a more balanced approach to inflation fears.

Just like balancing any portfolio, if you are all in on one narrative, you’ll be in real trouble when that narrative dissolves.

If you follow my newsletter you know that I prefer an approach where rates have lower volatility with a higher average level that is tied to some longer term measure of growth, whether it be productivity or growth.

Over-estimating the efficacy of monetary policy is a dangerous game, and if there is one good thing to come out of this inflationary episode it’s that central banks will try to take a more even approach to their ability to forecast – and the effect their tools actually have.

This analysis ignores one important topic I’ve raised before. The PBOC is a globally relevant central bank that continues to move interest rate policy in a different direction to the Fed and the ECB. Right now the currency is taking this divergence, but rates will find it harder to ignore this in the future. This will complicate any reluctance from the Fed to do extraordinary easing.

Calculating this probability involves some brave assumptions.

For the fair shape of the curve I have assumed the maximum of prior inversions for this part of the money market curve, suggesting 2 cuts over 2024 and 2025.

From here, I have assumed all future paths of forward rates are evenly distributed below and above this fair expectation, netting out.

This leaves the left-tail price indiscriminate buying which isn’t offset by similar selling from the expectation of higher rates, as indicated by the volatility smile chart in the prior section.

The leaves the probability of <1% rates anywhere between 12.5% and 25%, depending on assumptions. This range is still far higher than that implied by the options market.

Thanks 🙏 great post.

Absolute pleasure as always, easily my favorite substack. And free to boot. Thank you very much..

Praise aside, I'd be interested in your personal view on economics in general (in case you have one). Interesting economic thinkers, whether you're a Keynes guy or a Mises guy, or something in between. And maybe your opinion on the US before the FED, say 1800-1900, impact of Gold standards etc. Some food for an eventual post down the line maybe if it's not too far off your alley.

Cheers!