Why equities love the death of the business cycle

Reaccelerating stimulus, easing and low economic volatility will buoy equities and will keep short-vol popular

The levers and tools that are meant to rescue economies from the depth of recession are currently being used to smooth and extend expansionary business cycles. Emergency tools and their pre-emptive use have been normalised to avoid any possible market turmoil.

Continual stimulus from large deficits combined with a slashing of left-tail financial stability risks significantly reduces underlying economic volatility.

Lower economic volatility translates directly to risk markets exhibiting very low volatility, matching the environment for uncertainty. If you wonder how the S&P500 can have such small drawdowns and seem to perpetually grind up day after day, your answer is here. This equity return profile lends itself to high performing short-vol trades too – but this compounds risk, as we saw in August.

I named this Substack “Macro is Dead” because of this theme. The effect of the accelerating trend of influence by these tools, starting after the GFC and accelerating through the pandemic. They have destroyed the organic business cycle, and with it the efficacy of the data and leading indicators macro traders used to use to predict turns in the cycle.

This has also meant that the cycle has changed from a wave with a constant frequency and amplitude to one more like an erratic spring with a much lower amplitude. The business cycle naturally wants to go into a down-cycle, but the top-down tools arrest it, shunting markets from worry to elation in tiny windows of time.

Economic volatility has vanished

The level of economic data such as nominal GDP growth is important to markets as it directly describes at which rate the “pie” is expanding. This is clearly important to equity pricing.

However, I would argue that the volatility of those metrics is as, or even more, important.

When hard-economy measures are falling in volatility, or are stable at low volatility, there is little reason for risk premia, in whatever form, to increase. This means that large drawdowns in equity markets (expansion of equity risk premiums), along with rising implied volatility (increase in volatility risk premiums) are very unlikely.

Couple this with decent nominal GDP growth and you have the ingredients for asset prices that grind higher.

A simple representation of this metric is given below.

The lower the metric is, the more stable the macro environment is relative to the level of growth. These levels are as low as they’ve been since the housing debt fuelled days of 2005-07, matching 2011 to 2013 and 2017 to 2019.

In the two periods mentioned above, the S&P500 price return was 54.0% (Sep-2011 to Dec-2013) and 41.4% (Dec-2016 to Dec-2019). The second period is notable because it didn’t arise from a large drawdown, so is not a result of a recovery from a recession.

I’ve written another piece about how the political system is geared towards the reduction in volatility and uncertainty in the economy and this (rather than low interest rates) is responsible for ever rising asset prices. Stability encourages greater leverage and thus more debt, which again feeds into asset prices. This is a self-sustaining cycle.

I can’t stress how important this dynamic is now. With continued money creation (mostly through deficit spending and the associated debt) the natural tendency for the economy is to expand in nominal terms, and for asset prices to keep pace with that expansion.

Asset allocators need to keep buying for inflows associated with this expansion, and with little in terms of risk in the immediate future there is no incentive to down weight any risky asset classes. Will this create above-average yearly returns? Perhaps not, but it will reduce the likelihood of large and persistent drawdowns.

Most importantly, you shouldn’t be surprised with the daily grind higher in equity indices.

The equity market

The stability in economic data lends itself to this feeling that the amount of volatility in the economy has reduced, but it is markets that give the day-to-day reinforcement that this is the case.

While somewhat arbitrary, a measure of an extension of a cycle is by considering how many days since equity markets have experienced a negative return of some magnitude in a day or week.

Equity markets tend to go up over time, and this occurs during periods of economic stability and low volatility, interspersed with large drawdowns in short periods when economic slowdowns become self-reinforcing. The nature of economic cycles and the government’s interaction with it can arrest the accelerating decline in the business cycle, and we get a restart and recovery.

Using the measure of -5% return in any one week to reset the counter, the S&P500 has surpassed any continuous rally in the last decade at a total of 117 weeks.

The last longest continuous rally without a -5% weekly return was at 203 weeks, as the economy recovered from the depths of the GFC. The GFC is now a long time ago and was a much more serious contraction in the business cycle than the pandemic.

The market had a long uninterrupted rally before the GFC, starting from the recession recovery at the turn of the century, continued into the China boom and was finally supported by the 2005+ subprime driven expansion.

The 2000s rally, however, was shorter than that of the 80s and 90s. The 80s represented a transition period from the extreme economic volatility of the 70s (in terms of both growth and inflation). As a result, equities had a very long unbroken period of positive returns. The 90s were the next leg of this trend, achieving economic volatility on par with pre-GFC levels. Both of these periods were matched with large debt growth.

Moving to return based analysis, the current rally looks even more favourable on cumulative (price) return.

When compared with the 2000s and post-GFC equity rally which were nearly 2x and 3x the duration of the current rally, the current rally has achieved more than two-thirds of the return of those episodes.

So, it is not only the duration of the current rally which is meaningful, being the longest in over a decade, but its magnitude is similar to that of a recovery rally out of a recession, without a recession ever occurring (remember that the current rally began in 2022, not in 2020).

Given the stability of the economy, the lack of a justifiable path towards recession and the Fed’s lock on financial system stability I would suggest that this has a lot longer to run.

If nominal GDP growth can continue to print above 5%, we can easily add another cumulative 20% to the current rally to match the 2011 episode. The basis for this outlook is the effect of a continuation of large deficits having a close correlation with nominal GDP growth, and thus the perpetuation of the current episode of extraordinary stability.

A key reason for the length of the current rally was that the Silicon Valley Bank crisis didn’t end up disrupt it. No interruption occurred because of the power of the Fed’s balance sheet to new facility construction to avoid financial calamity.

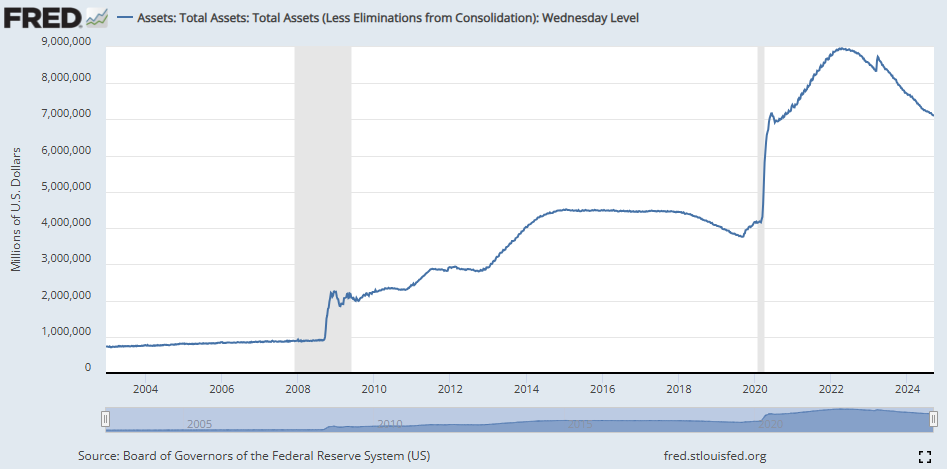

The Fed’s balance sheet size controls financial sector risks

A lot of people mistake the difference between of the Fed’s balance sheet pre-GFC to now as the result of continuous stimulus into the economy. This isn’t true.

Concentrating on the specifics of the composition of the Fed’s balance sheet can cause us to miss the real reason that it is as large as it is – shifting regulation from the fallout of the GFC forced put the Fed in the position of the main intermediary of the financial system.

Basically, the Fed’s balance sheet is huge because operating as this intermediary requires balance sheet capacity.

Bank reserves increased partially due to QE and partially due to a mixture of new regulations introducing restrictions that constrained the ability for banks to easily fund themselves for the very short-term (via repo or money market instruments).

These restrictions affected those that funded banks for short-term shortfalls, who now had far fewer assets that they could invest in. This reduction in assets was compounded upon by regulation stopping money market funds from being able to purchase short-term bank issuance, limiting the bulk of money market funds (with the prime designation) to government debt.

These changes created a gap in the middle that the Fed, whether by intention or not, had to step in to “manufacture” the same assets that the banks did so that money market funds could continue to exist.

The net sum of these regulations has stopped banks “manufacturing” short-term assets needed for the financial system to work. Instead, the Fed transforms US Treasuries and bank reserves into the required short-term assets, backed with the unquestionable credit quality of the Federal Reserve and the US government.

Additionally, the time it takes to deploy further balance sheet resources to stave of any sort of financial crisis similarly seems to be getting shorter. The Silicon Valley Bank crisis birthed the BTFP facility that allowed small banks to effectively borrow against their discounted US Treasury holdings to make up for any funding holes due to deposit runs. It was set up in an extremely short period of time, surprising given that the Fed was lending to troubled entities at a greater amount than the market value of the collateral provided.

The intent of this behaviour is clear to me. The Fed has been comfortable with taking the role of intermediary purely to avoid any chance of financial calamity. It continues to be ready to deploy more balance sheet to achieve this outcome.

The SVB crisis is partially the fault of huge pandemic-era government debt creation, and a lack of oversight from treasury desks at the banks and regulators recognising the risk of the now large amount of interest rate risks at these banks.

Maybe the outcome would’ve been different if it was private lending, rather than government debt, that caused the capital issues.

The vol spike we had to have

Stability by diktat doesn’t prevent equity markets from having their occasional violent (and very short lived) bouts of volatility.

August’s drawdown is a result of both:

A temporary lull in deficit spending; and

The popularity and the inherent instability of the short-vol trade.

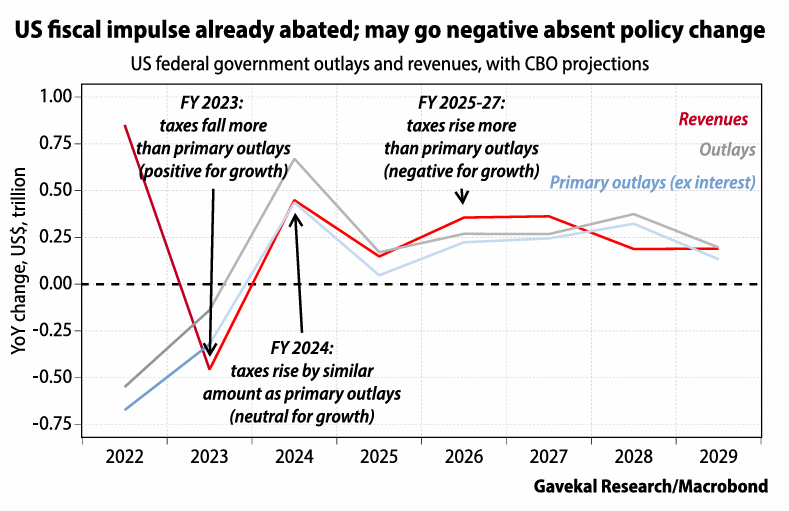

From a primary deficit standpoint, revenues (in the form of tax take) for the US Federal Government have increased relative to outlays since about the end of the 2nd quarter, reducing the fiscal “impulse”.

This lines up with my US debt growth to S&P500 equity predictive model, which uses the pace of debt growth across public and private debt to predict periods of market volatility. I outline its construction in this X thread here.

This predictive capability of this model is based off the change in pace of debt growth, rather than the outright level that the GDP model does. From this perspective the slowdown from the incredible growth in new money making its way into the economy from the highs of 2021/22.

The indicator is normalising and will be long equity soon, indicating that the market should be set for further gains (the model will buy equity again once the indicator is above the red line).

Debt growth slowing as it has made equity markets more two-sided than it’s been for a long time. It’s this more balanced two-sided nature of equity price moves that opened the door for an earthquake, with the epicentre being the short-vol trade.

The short-vol blow-up

When I talk about being “short-vol”, I’m specifically referring to trading volatility directly, either through variance swaps or the more popular option – VIX futures.

In short, these instruments allow a trader to take a position on the implied volatility of a market, in this case through the VIX index itself which represents a basket of options across different expiries and strikes.

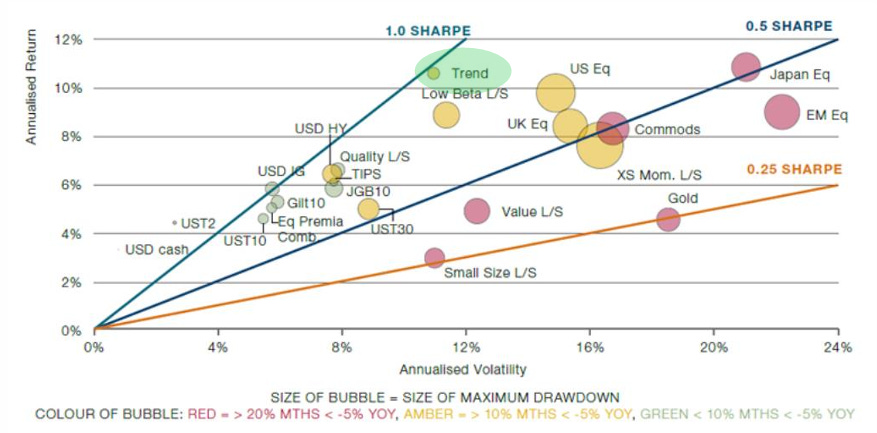

The popularity of these futures has increased rapidly in the last few years because of the potential risk/return outcome available in quiet times. The chart below shows the rolling 1-year Sharpe ratio for the 1st and 2nd VX future.

This instrument has spent ~1/3 of the time since 2011 producing a Sharpe ratio of >1.5. There aren’t many assets that can produce this sort of risk-to-return for sustained periods of time with a pure passive-only buy-and-hold investment.

The only asset class that gets close is credit, with high yield delivering ~16% of samples above 1.5 Sharpe.

This shouldn’t be a surprise as they are both an estimation of the underlying volatility of the assets of the companies within their respective indexes. The shapes of the charts are very similar as a result, and the events that cause Sharpe ratios come crashing back to earth when a volatility event occurs. Both are also as illiquid as each other when these events occur.

The persistence of long periods of high return-to-risk means that disruptions must occur regularly enough to bring the average risk-to-return to a more normal 0.5-1.0 range, matching most other asset classes.

If any asset class had a persistently higher Sharpe ratio than the rest, then something must adjust to cause the long-term Sharpe to move to closer to the historical average. If it didn’t then capital would flow to close the gap, assuming some level of efficiency.

In corporate credit the adjustment occurs as above-average returns will cause capital to flow to the sector, eventually increasing bad lending and increasing defaults, destroying that capital. This will act to bring down average return-to-risk ratio.

The equivalent of defaults in corporate credit when trading volatility are mark-to-market losses. These losses are crystallised at the expiry of the derivative and as such can’t be avoided.

Therefore, as more capital piles into volatility the mark-to-market loss in an event of instability will have to adjust to the amount of excess capital that has driven an unbroken run of strong returns. The magnitude of the carnage that occurred in August is a direct result of the strength of the returns in the period before it, as seen in the chart below.

The price chart above shows the run up to the August 2024 and January 2018 vol blow-ups. Both had a period of above average performance indicated by the arrows, and both periods lasted about 2 years and experienced a vol spike of about 50% of the prior cumulative return.

The extreme relationship between price action and liquidity means the event itself is truly random. Only the smallest perturbation is required to cause an explosion because of the inherent unstable nature of short-vol positioning.

In this case it was exacerbated by a low-liquidity Asian trading session and a fear about Bank of Japan rate hikes into a market that was already down sharply from its high. The unwind of the FX carry trade reasoning popular at the time was merely a red herring.

Carry is usually great, until it isn’t. Unfortunately, it must be that way, and the capital flowing towards it will make the blow-up is a certainty.

Where are we left?

The market’s changing opinions on the turn in the cycle seem schizophrenic and lead to a very fast recession/no-recession reactions. Don’t overreact either way. The support for the economy is still there and will likely reaccelerate by the start of next year. How interest rates trade is up for discussion, but the buoyancy of the equity market isn’t.

Can weakening labour markets upend the stability? Or are subtly weakening labour markets a symptom of an extended cycle that has already amassed a lot of waste? My bet lies with the latter, with employment markets waiting for the fiscal impulse to resume to get “unstuck”.

This all leads to ignoring the US as the catalyst for the return of business cycle downturn. The election outcome will be irrelevant from the point of view of the size of the deficit. Neither candidate has enough political capital to attempt to accept the economic consequences of trying to balance the budget.

The direction of your concern should be China and Europe. Neither region has the same amount of fiscal support while having much more serious underlying economic issues.

Europe needs a far deeper look, something that I will leave for another newsletter.

The real question is if these worries enough to derail risk appetite for now. I don’t think they are, yet.

Very interesting and a useful challenge to my thinking. The problem I have is that valuations on most metrics are somewhere between very high and impossible to sustain, GDP growth is low, Gvt debt is high. So buying equities feels like a trade that is contradicted by the long term fundamentals. Still, I suspect that, at least for now, the argument he makes for equities grinding higher might prove sound. I just can't bring myself to buy. Perhaps that thinking by others is why they will grind higher.

I'm not a believer in velocity as an independent variable. To me it's an error term that sits between GDP and whatever measurement you use for money supply (which is generally M2 but this isn't always the best indicator either).

I've seen Bob's argument, and I think that's the step past debt growth which I think is more relevant. The debt growth enables income growth because it promotes persistent excess demand which drives activity (profits, employment, wages, the whole lot).