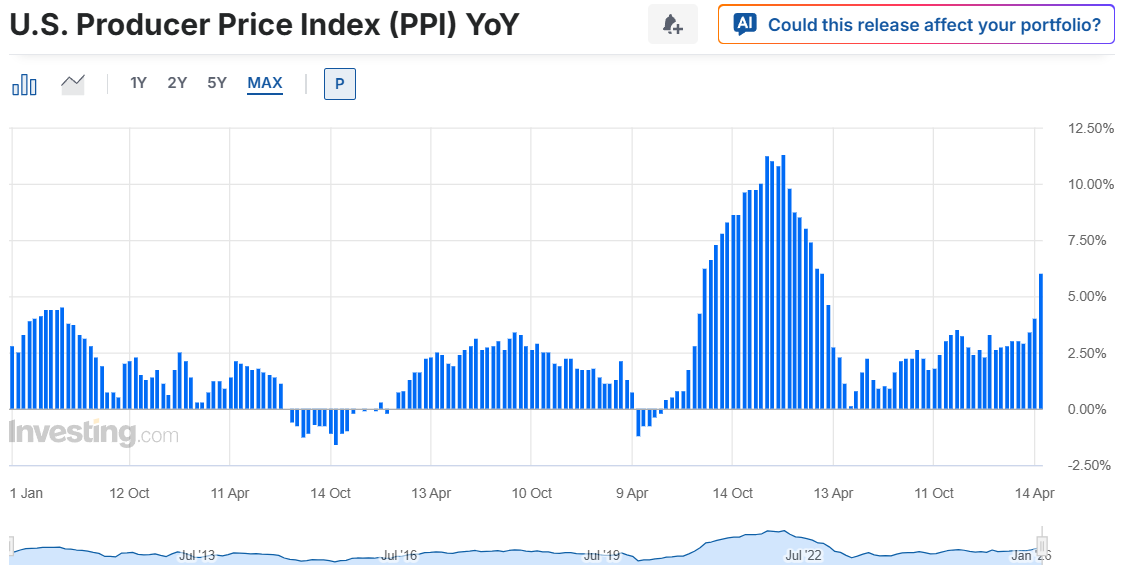

Last week’s US Producer Price Index (PPI) print in the US finally got me off the fence on bonds again. I sold a third of my max risk across the US, UK and Europe, looking to add more on a bounce. It didn’t take long but the 10% rout in crude (and a soft UK CPI) has already given me another look at it.

To be clear. I don’t think the levels to sell here are particularly good. Kevin Warsh will mean that not hiking will be considered the equivalent of trying to force hikes through the board.

The Europeans already have enough priced in that a short trade in bonds isn’t a play on pricing or curve dynamics.

What a short here is a play on the return of a 2022 like trend in rates. The longer that the Iran situation drags on, the greater the effect on pass-through inflation to an extreme point. The probability of that has risen, and it offsets the poor levels for entry.

Reducing it down to the Strait opening or not ignores this fact.

Avid readers would have noticed the continual promise to do a rates market review, and I’ve continued to put it off. There are a few reasons I had to be brought kicking and screaming to put on rates positions again.

My main models have performed horribly since 2022.

US rates have become overtly political (not that they weren’t political before, it was just silent).

30-year yields have been targeted for various reasons (some political as well). This places a natural barrier on shorts across the curve.

Being short bonds is hard. Being long bonds is useless in the new world. Why bother?

If you are going to bother, be sure why. Is it an alpha trade on its own, or will it fit in with equity or commodity exposures?

Rising yields on an intrasession basis has been correlated with falling stocks. On a longer window stocks have been ignoring rates after what has been a huge shift in expectations for the Fed Funds pricing.

The chart above is the best analogue for what could be the current care of the equity market. US 30-year yields rose 1.7% from 5% to 6.7% in the mania portion of the dotcom boom.

This gets to the heart of how people are seeing this market. Is it oil driven inflation, or an AI driven overheating US economy pushing global yields higher? How does the flagging EU and Asian economies fit into this?

No trend to follow with no cycle

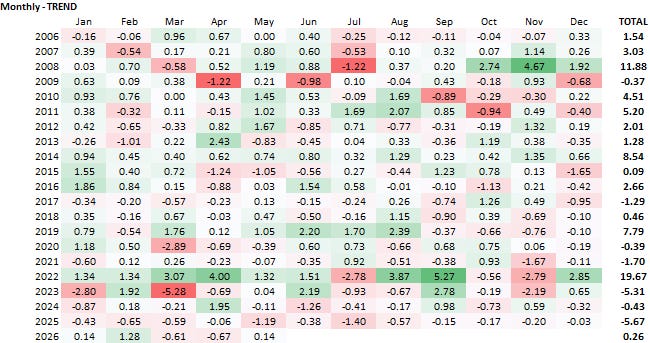

Below are the returns from a simple trend following model in global rates.

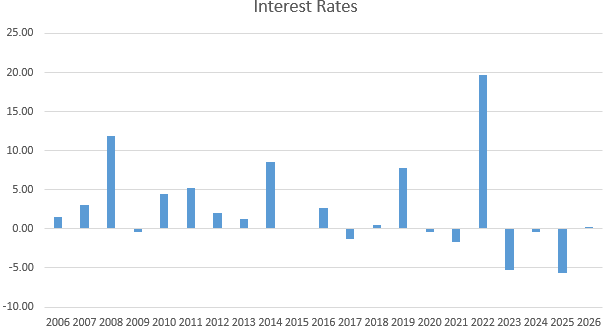

The big returning years, 2008 and 2022 at 12 and 20% respectively, offered the biggest opportunity due to a large trending move lower and higher in yields. Both were useful against a portfolio of risk assets.

If you want an explanation of why this model works, see the write-up below.

Outside of 2008 and 2022, the model performed well as bonds were broadly in a bull market from 2007 to 2019. If we exclude 2022 as a unique event, there has been no trend in bonds since 2019. Even 2020 didn’t work well despite the fall in yields to all-time lows.

2022 was meaningful for the bond market. It was the end of disinflation as a theme, and with that the default position for a central banker since the turn of the century ended. No more insta-cuts when growth or equities falter.

This coincided with the end of the business cycle as a result of fiscal largesse. Avoiding a recession was policy now, no matter the cost.

With that we saw the end of trending bond markets. 2023-24-25 saw consecutive losses for a model that performed well (and has been out of sample) since 2012. Out of sample is less relevant for this model and it is specifically tuned to capture the big cyclical moves in rates rather than smaller trading cycles (although components of it do capture this).

This alone tells you that you are in a mean reverting market. A market for traders who like picking the turns, or playing curves, or trying to scalp the front-end. This isn’t the market for someone who wants to use bonds as insurance.

I’m really only interested in a big move. The possibility of that has increased substantially even if entry levels aren’t great.

Why now? You’ve missed the whole move

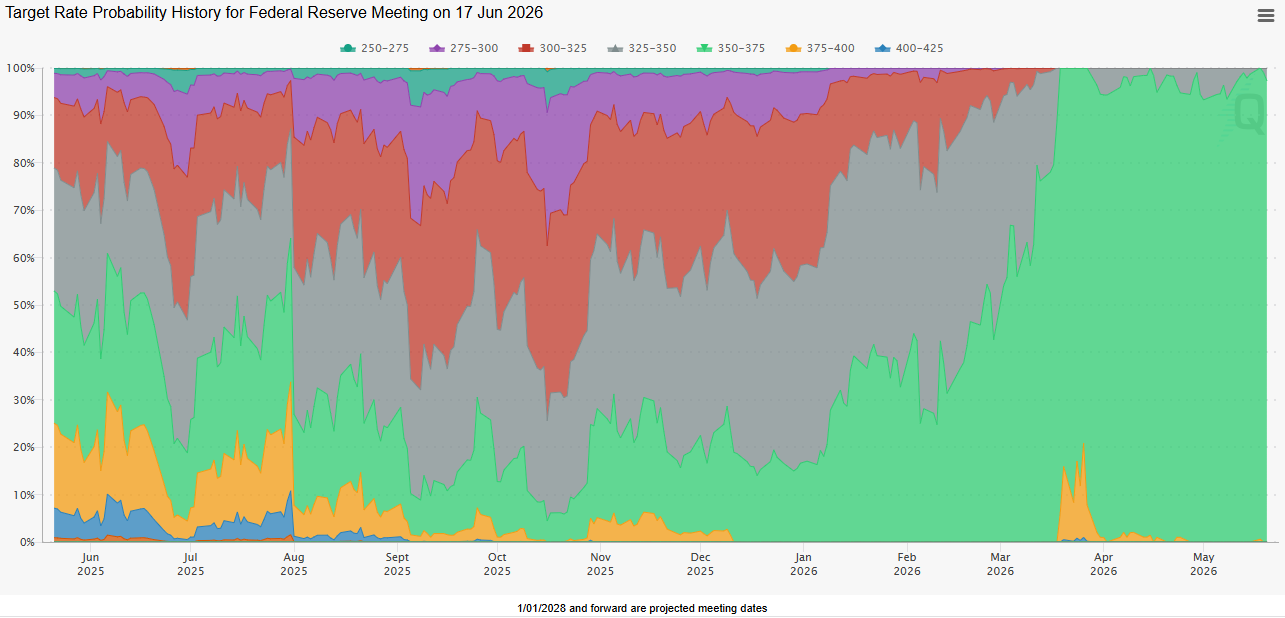

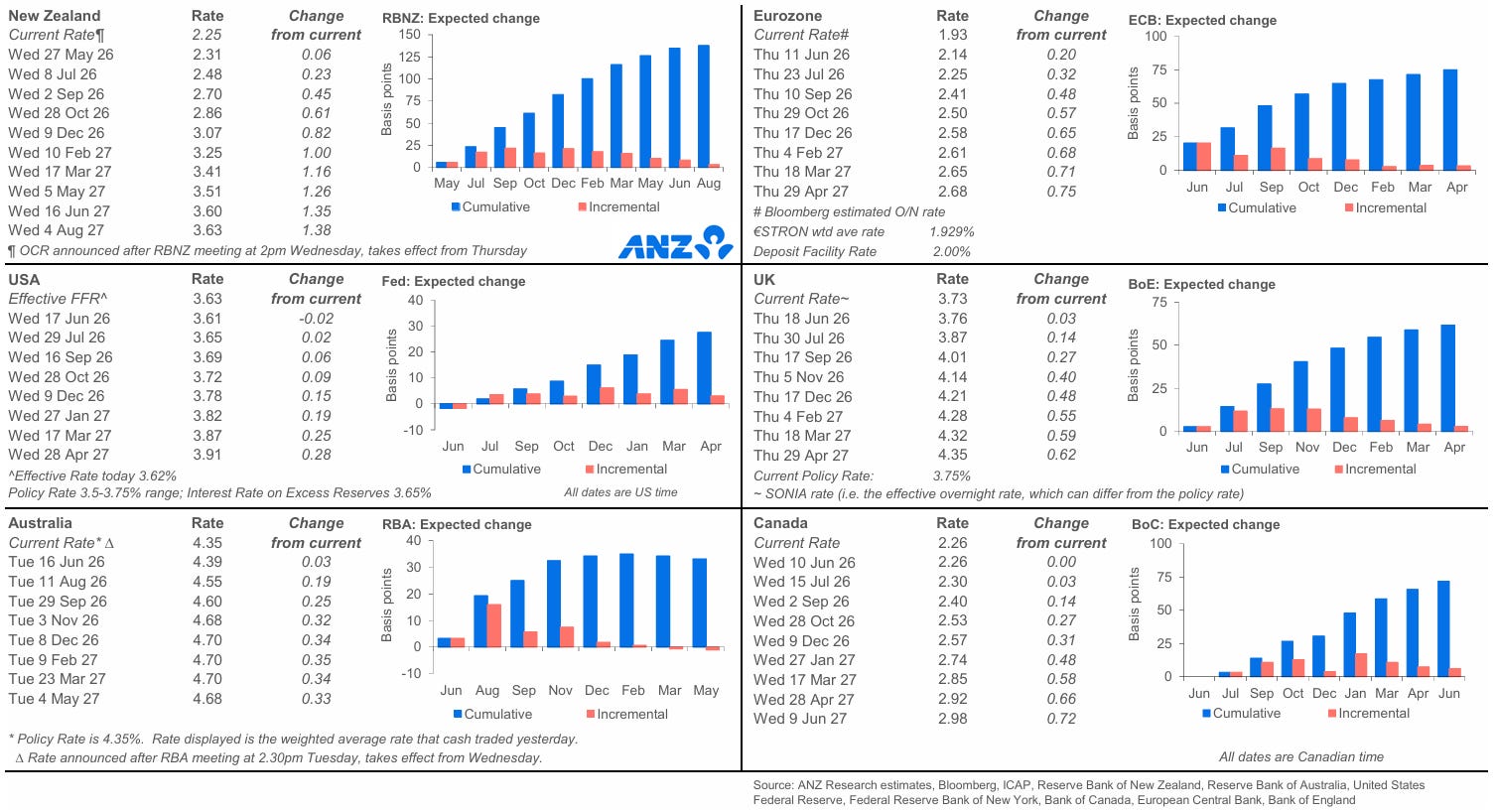

Pricing has moved a lot, especially in the US.

The June meeting went from an 80-90% chance of some sort of cut to now being a priced in hold.

From the peak of rate cut expectations, Dec-2027 SOFR has completed a near 1% turnaround.

Visualised as a curve is even more stark. Note the “hump”…a small hiking cycle which resolves itself quite quickly.

This small hump leads into measured hiking expectations despite the outright shift in expectations. 2022 this isn’t. The ECB is slated to hike in June, but after that there is another 2 hikes into the middle of 2027. For the US, the market is unsure about even 1 hike, or roughly the 50% chance of a hike by October this year.

The divergence is in economic performance

Oddly, rate hike expectations seem to be clustered towards those economies with the weakest performance.

Australia (including 2 delivered hikes) > EU > Canada > UK > US.

The first 3 aren’t too different to each other, each pricing in about 3 hikes.

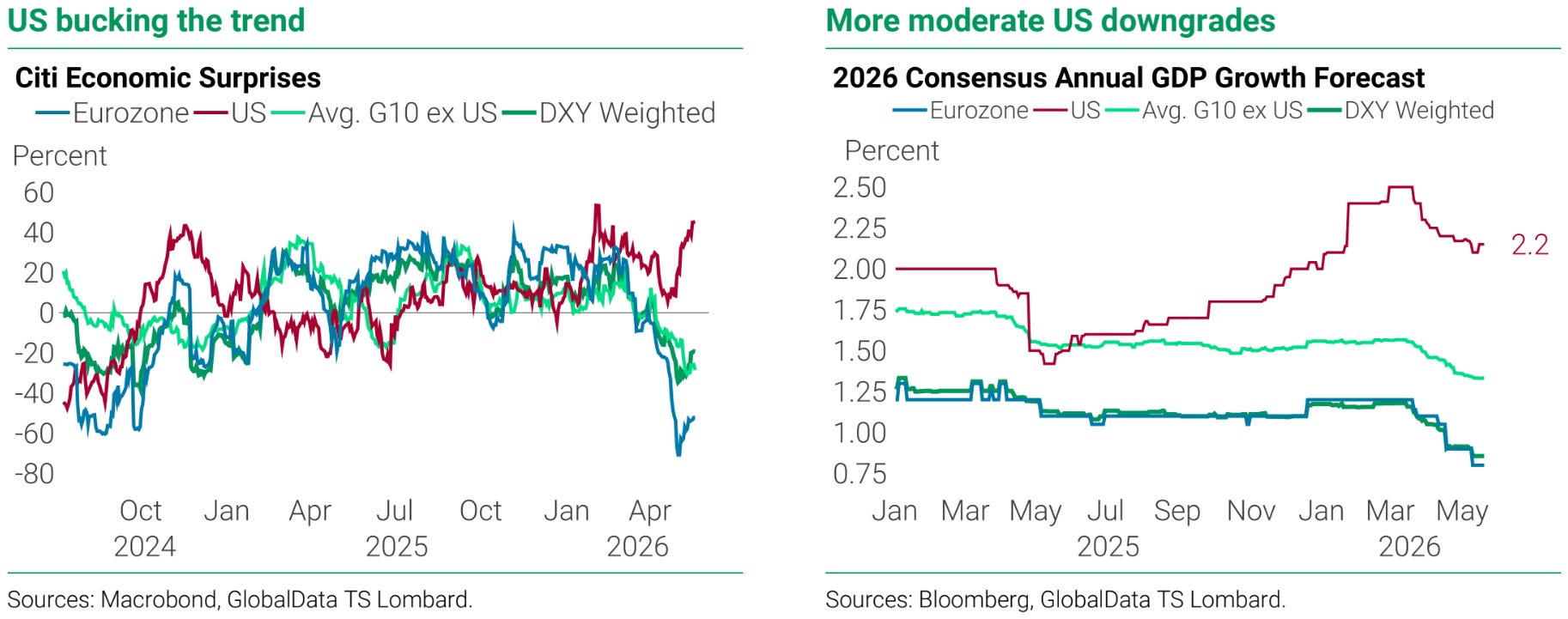

Economic surprise indexes and outright growth levels highlight a huge divergence.

Even the US labour market which was expected to at least print some poor outright figures (without a rising employment rate) has improved on that front, too.

The themes for GDP growth in the US remain the same. Investment continues to drive good outcomes. Large US oil export volumes will flatter this quarters GDP, too.

Then you have the flipside across the Atlantic. Growth was poor coming into the war and has only worsened. Last week’s PMIs were a horror show. These are recessionary levels.

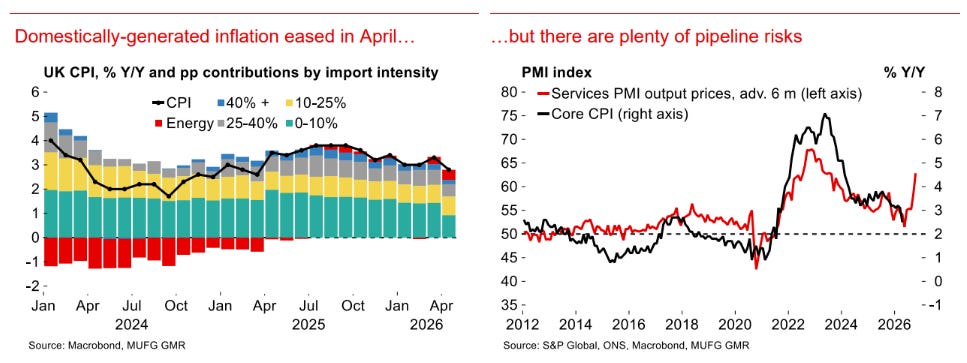

The UK printed a weak CPI last week. But as with Europe in the chart above that, pipeline risks are there.

I started this piece with the shock of the US PPI print. The PPI is historically a poor predictor of CPI but is useful if you only consider the error to expectations as a guide to the error in underlying CPI.

The truth is that there is still some residual disinflationary pressure within US core CPI, with OER still trending downwards.

There is also little doubt that the US isn’t as exposed to inflationary pressure as Europe and Asia are. Gasoline prices are one thing, but the US’ cheap and abundant natural gas means cheap and available feedstocks for her petrochem industry. It’s through this channels that I worry most for inflation upside, outside of food costs.

30y has captured the headlines

The 30-year point of the curve is its own beast. Driven mostly not by inflation expectations or central bank policy settings but by demand of the institutions that use them for liability hedging. They are more of a tool than the rest of the curve is.

Below is a piece I wrote pushing back against the panic about 30-year rates exactly a year ago.

Charts & Notes: 30Y JGB(edlam)

There is one thing that is true in every bond market - the 30-year point on the government yield curve is its own beast driven by buyers that aren’t dictated by price but rather than need to hedge their liabilities.

The market does take notice when they start moving though.

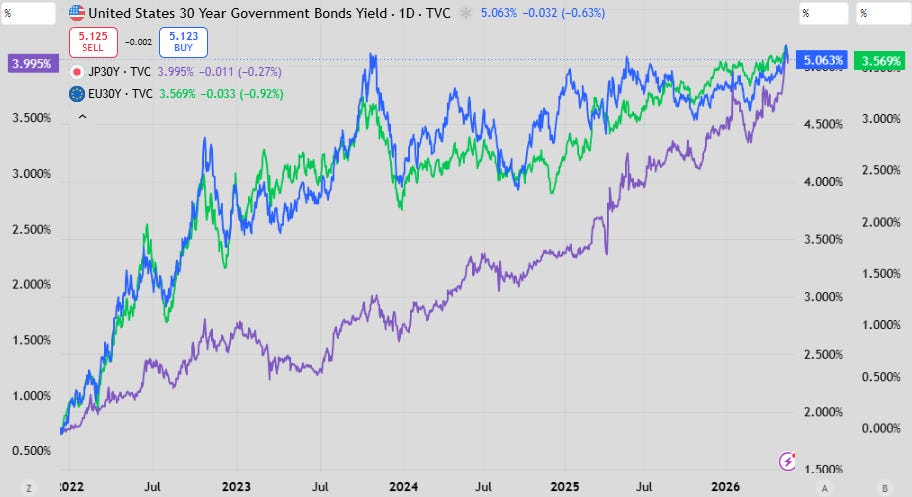

That article a year ago marked the top in the steepening of the 10y/30y yield curve. 30-year rates are much higher in Japan (from 3.15% to 4%) but it isn’t the long-end of the curve that is leading it.

This is why you expect the curve to flatten as rates rise (and steepen as rates fall). This is normal behaviour and it is the shorter end of the curve that is driving these moves.

News outlets still focus on their headlines on the 30-year bond. Modern politics outside of Japan freaks out when it gets too high (interestingly westerners are more worried about the 30-year JGB than the Japanese are).

Make no mistake though. The 30-year isn’t the tail wagging the dog. Rising inflation expectations have been the culprit. Worrying about the 30-year specifically isn’t the right way to look at things.

Why isn’t pricing favourable?

Current yield levels aren’t attractive for shorting on their own.

To keep it brief, there are 3 reasons for this:

The rate hike cycle in 2022 was difficult for central banks. Doing it a second time will be a real struggle for them.

Growth is already in a much worse place outside of the US (where it is genuinely good). This will play into #1.

Populism is far more progressed than after the pandemic. This will push against hikes aggressively.

These factors make a delayed start to a cycle likely. This moderates short-end pricing and makes current pricing not the best you’ll get.

If you want to jump in a what could be a very large trend move sometimes it’s best to just get started with it.

Great read!