A guide to (inflationary) money printing

If QE isn’t money printing, then what is?

This newsletter establishes the two conditions that define what true inflationary “money printing” is.

The first condition is that a central bank must create liabilities that cause a depletion of its equity, implying that money creation is unbacked and unsterilised.

The second condition surrounds the ability of the money created to be spent in the real economy on goods and services, such that it can create inflation.

Under these conditions, Quantitative Easing is not inflationary money printing, while paying excess interest and debt cancellation certainly is.

My last newsletter analysed past Quantitative Easing (QE) episodes and concluded the effect on markets and the actual economy, including growth and inflation, is extremely limited, despite the eye-popping sizes of these programmes.

The effects of QE are muted because of the “sterilised” nature of bond buying and the limited effect of it outside the banking system. The bottoming of risk markets that tends to coincide with QE is due to the fiscal expansion that occurred parallel each of these large QE programmes, rather than QE itself.

This is not what you would expect from a central bank action that many call “money printing”. QE doesn’t actually fit the definition of money printing that most hold, which includes that it must debase the currency and cause inflation.

Central banks can, however, take action that results in inflationary money printing.

Real money printing looks a lot different to QE, and this newsletter will show how to spot if a central bank is actually printing money that is unsterilised and to identify how it enters the real economy. Money may be created out of thin air, but it still needs to be spent on real goods and services to affect inflation.

How money is usually created

Most people know that the money creation process occurs through commercial banks, but don’t really understand how. The days of fractional reserve banking were over a long time ago, and as such there is no link between deposits and the ability for banks to create loans.

Modern banking uses the idea of loss-absorbing capital, which can take many forms. A bank requires a certain amount of capital to make loans so that it has sufficient buffers to deal with bad lending, with the sufficient amount set by the banking regulator in that country. For the US, the Federal Reserve sets regulation for large commercial banks. If a bank wants to lend more, it can just raise more capital. As long as it can do this, there is no limit to lending.

How is money created through lending? When a loan is made, a deposit is created simultaneously at the same bank for the loan amount. From here, that new money is able to be paid towards whatever purpose the loan is for. If it’s a mortgage, the new money will end up with the vendor of the house and now it is out there in the wild, circulating around the economy.

This process does not require an existing deposit to pay the vendor, as that money is created along with the debt. The commercial bank’s ability to magically conjure into existence an electronic version of the US Dollar sitting in a deposit account is how they create money.

Their capability of a bank to be able to determine credit risk and collateral value is why they are entrusted with creating money. The idea is that the bank, as a private, for-profit entity, would never risk its own capital to lend and thus create money without evaluating the risk of bad lending properly. This method of money creation isn’t inflationary (when done properly) as new money is created when new, productive assets are added to the economy. Essentially, the amount of money grows with the size of the productive economy.

This idea works as they only lend against economically valuable assets and businesses. Of course, there are many examples throughout history of banks getting it wrong, and the resulting loan losses end up destroying money in a very painful process.

It may not be perfect, but the current system deals with the responsibility of money creation of a growing economy by forcing that upon the private sector that should see incentives aligned, and therefore the best outcome achieved.

How central banks create money that ends up in the real economy is very different.

QE is not money printing as it does not create real-world money

QE does not result in money creation, even though it seems analogous to the way commercial banks create money. The Fed creates liabilities just as a commercial bank does to enable it to buy government securities. This seems the same, but it isn’t.

To understand why it isn’t money creation, we need to understand how bank reserves work.

To pay for the Treasury securities it buys under its QE programme, the Fed creates liabilities to buy those assets that are accounted for in US Dollars, in the form of bank reserves.

At first glance there is a lot of similarity with commercial bank lending, since bank reserves are deposits for banks just like bank deposits are for individual citizens and companies. However, there is a difference.

The bank reserve that a commercial bank holds on its balance sheet is the payment for the Treasury security that it sold to the Fed. The Treasury security was already paid for by the bank using another funding source, or a mix of funding sources.

This bank reserve isn’t a profit for the bank. It’s merely payment for selling a security, in the same way it would do it with any other counterparty. To the bank the reserve is just payment for money it has already spent. This means it is not a windfall that can be paid to shareholders as dividends, or employees as bonuses.

This reserve can be lent to another bank if it sees a better opportunity for this money. Since interest is paid on reserves, there are few other opportunities than Treasury securities to invest into, making the existence of the option to lend reserves academic.

Bank reserves are essentially locked until the Fed decides to reverse QE, and reduce the Treasury securities it had previously bought from the banks that own those reserves.

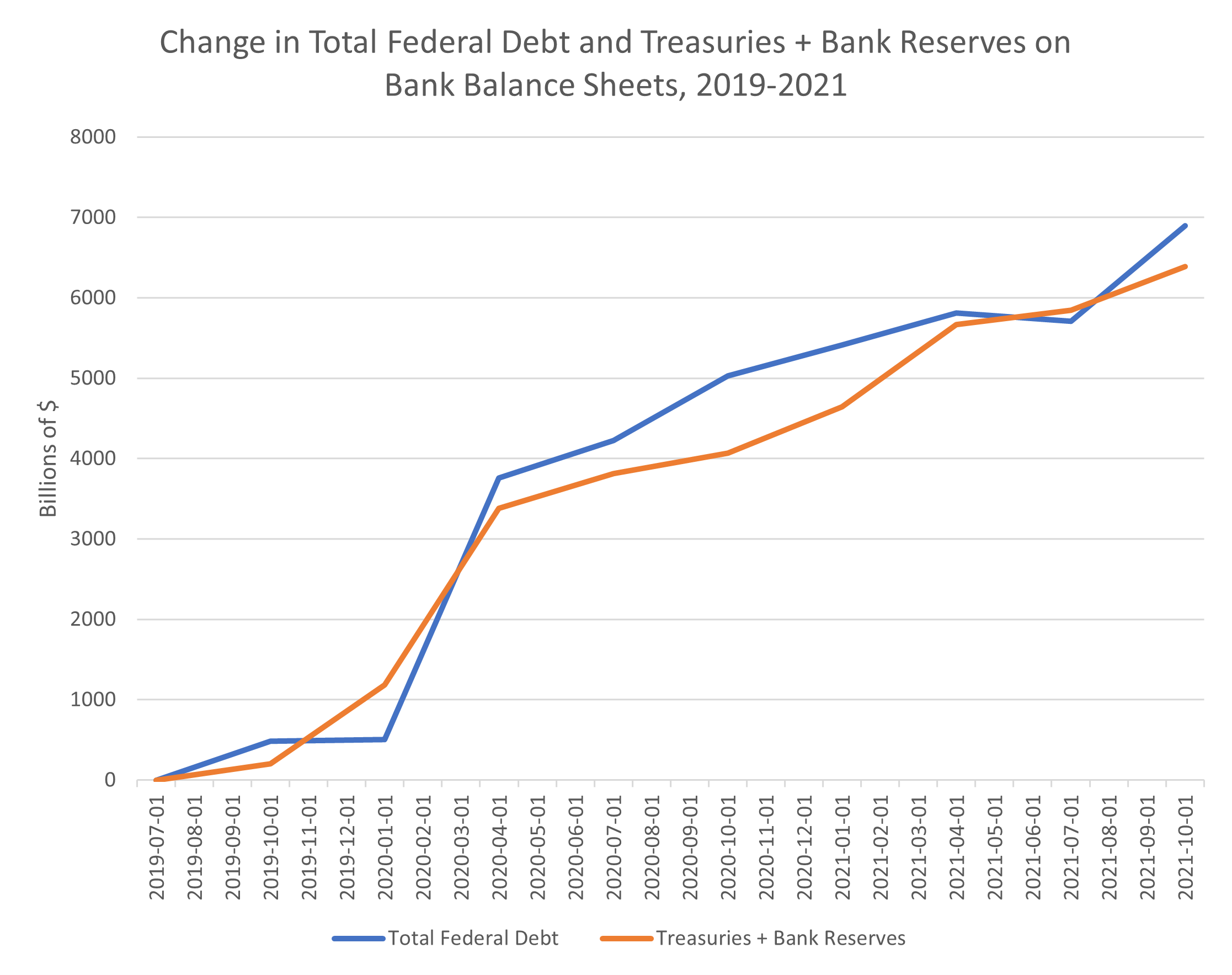

It is the initial purchase of the Treasury security (usually on issuance from the government itself) that creates the money necessary for the government to pay its stimulus. The chart below highlights how quickly the banking system expands its balance sheet for new government issuance. Deposits follow the same trajectory, climbing by $5trn over the same period.

QE occurred at a much slower pace over the pandemic period, countering claims that they “funded” the government. The banking system funded the government, as it always does, creating money in the process.

Inflationary money was not created by the Fed, but by the government expanding the deficit and banks creating the money to fund that. The true “money printing” came from new debt, just like it does when a bank issues a new loan.

Central bank money printing happens in another way

The trillions in QE we’ve seen so far is not considered to be money printing in terms of debasement, and therefore doesn’t drive inflation. This doesn’t mean that it is impossible for a central bank to create money and expand the money supply in the way most people consider it.

To know when a central bank is printing money, we need to keep a close eye on their equivalent of capital for a commercial bank.

This may seem odd, as the capital (or equity) component of a central bank’s balance sheet is not of much concern and not given much attention, as there are no immediate consequences to a central bank in negative equity. Negative equity won’t bust a central bank like it will a commercial bank.

Watching how the equity component changes, however, is the key to knowing when a central bank is actually printing money, and when this money may have an effect on inflation.

The nebulous idea of central bank equity

Central banks have equity just like a commercial bank does. It’s just not very much. The Federal Reserve runs with less than 0.5% of equity, against the 7-12% a typical commercial bank does.

The Fed doesn’t need much equity because it doesn’t have lenders like a commercial bank. A bank needs to convince its depositors and debt holders that there is sufficient capital to absorb losses and to make sure their money is “safe”.

A central bank doesn’t care about its liabilities, because it can just create more of them at the press of a button. Every counterparty to a central bank can always be made whole, with just a few keystrokes.

Like a commercial bank, the Fed can make a profit too, which positively affects its equity. If the average coupon rate of its asset book is higher than the rate it pays on liabilities then it will book a profit in a given year. The Fed is required to transfer all of its “profit” after costs to the US Treasury each financial year. They paid $107.4bn to the US Treasury in 2021, and have tended to make profits every year.

The Fed can also make a loss, however. This is where things get interesting.

The Fed are printing in small size, right now!

The Fed’s equity buffer is depleting at the moment, with those losses being booked as a “deferred asset”. A falling equity buffer is a sign that the Fed is releasing unbacked new Dollars into the market.

Fortunately it is small, and not really of any major relevance. It will also likely rectify itself as the Fed finishes hiking (and even faster if they cut rates).

It is, however, a great illustration of why equity matters.

This article details the losses being experienced by the Fed at the high level, and are correct in saying that it was expected. Like any simple bond portfolio, we can forecast the revenue to be made from coupons.

As at January 4th, 2023 the Fed owns Treasury securities that are distributed by maturity as per the chart below.

Since the growth in the Fed’s balance sheet occurred when the yield curve was depressed (2020-21), with Fed Funds at 0% and the 10 year bond anywhere between 0.7% and 1.5%, we know that the average coupon on the bonds they acquired was very low compared to the Fed Funds rate today (~4.3%).

As 2022 passed, the shorter duration bonds have rolled off the portfolio and higher coupon bonds would’ve been bought, but the average would still be very low as half of the book consists of bonds with a maturity of greater than 5 years.

The liabilities on the Fed’s balance sheet are much shorter duration assets (mostly 1 week to 1 month) that have almost fully adjusted to the much higher Fed Funds rate. The Fed pays interest on these liabilities at roughly the Reverse Repo Facility Rate (RRP).

However, the liabilities on which the Fed pays the RRP rate makes up only 70% of the total. Physical paper currency on issue is a large component which has no interest cost and this reduces the average payments significantly.

Once we apply some math here, taking into account interest free liabilities, the current breakeven rate on the Fed’s securities portfolio is somewhere around 3%. While I’ve only considered Treasuries in the previous chart, the Fed also owns other securities, such as mortgage-backed securities, which pay a credit premium as well. These securities will lift the average coupon rate, but not enough to get to 3%.

Therefore the gap between payments and receipts is quite large. It has led to net income losses as plotted in the chart that you see below.

Earnings remittances that normally go to the US Treasury hover at around $2bn per week. Today, these have plunged to -$2.5bn, and this figure is climbing.

This equates to an annual loss of $130bn. Working backwards, this loss equates to a shortfall on the securities portfolio of 1.3%, putting the realised average coupon on the portfolio at roughly 1.7% today. This is entirely within the expected range for the portfolio, given the period of acquisition and the time that has passed since.

There is nothing sterile about losses

The other side of net income losses is that there is an equal amount of money that is ending up in the private sector as an interest payment well above the equivalent payment if they had just taken the risk on the Fed’s underlying security portfolio.

These payments to the private sector can’t be mopped up by the Fed at a later date. They can’t sell anything to the banks or money market funds hoping to reverse these injections.

The only way they can be reversed is through the Fed making a profit in the future to offset these losses, and work its way out of negative equity. This is not guaranteed as it will depend on the level of short rates versus long rates, something the Fed does not control.

To be fair, this amount of unbacked stimulus isn’t all that much. $130bn per year is about $10bn per month. This is in the context of $200bn per month of new private sector credit created through commercial banks, so it is fairly irrelevant.

However, it is still money printing, and debasement of the currency, just on a very small scale.

Knowing how the accounting works in regards to a central banks equity is vital to know when a central bank is printing money without any ability to mop up that new money and reverse any stimulus.

The ultimate way to create negative equity

Net income losses on the books of a central bank might be a fairly innocuous version of money printing without too much ability to create serious debasement.

The extreme version of negative equity creation is through outright cancellation of government debt by a central bank.

Debt cancellation has been theorised as a way for Japan to get out of its extreme government debt situation, a relic of the bust in the ‘90s and the stagnation since then. The Bank of Japan owns roughly half of Japanese government bonds on issue, with nearly all of the rest owned onshore.

Debt cancellation is the process of a creditor saying to the debtor that the debt is forgiven, and does not have to be paid back. The accounting for this process is similar to a default. The creditor will eliminate the asset (being the loan) from their balance sheet, with a loss being recognised through a decrease in equity (through a reduction in retained profits). The opposite would occur for the debtor, with a profit being realised, lifting equity balances.

Obviously the concept of “equity” for a government is not relevant, but the effect would be represented as a massive expansion of borrowing capacity.

Using the rule around the creation of negative equity, the debt cancellation process would constitute outright money printing by the Bank of Japan. There aren’t many people who would disagree with this.

Debt cancellation is a non-cash accounting event, however. How does it then become inflationary?

The net income loss situation for the Fed has a clear transmission path to the private sector through increased interest payments on its liabilities. This is a fairly obvious transmission mechanism for the new money to make its way into the economy.

For debt cancellation, the path to inflation may seem to be through reduced interest payments, but that isn’t the case. Interest payments by the government are recirculated back through payments by the Bank of Japan, meaning that nothing really changes here. Elimination of interest payments has no monetary debasement or inflationary effect.

The truth is that debt cancellation doesn’t actually do anything in the first instance. The non-cash accounting entry associated with debt cancellation means that the temporary increase in the money supply by the central bank is now just made permanent.1

We have argued, however, that negative equity on a central bank’s balance sheet is indicative of money printing. So how do the stimulative effects manifest themselves in the example of debt cancellation?

The stimulative effect is in the subsequent behaviour of the government concerning its fiscal policy. In effect the central bank is facilitating the creation of new money by the government through further debt expansion that it wouldn’t have done otherwise.

In the extreme example of full cancellation, the Japanese government will go from being burdened by debt totalling 263% of GDP, to a fresh balance sheet with no debt. What government could possibly resist spending in this environment? Even a large continual deficit of 5% of GDP, it would take 50+ years to reach the OECD average for government debt to GDP (~110%), with growth offsetting some of the debt increase in that time. This would lift the wealth of Japanese people immensely, and is equivalent to the monetisation of a demographic dividend.

It may also lead to runaway inflation that takes more than it gives.

Money printing can take many forms

The term “money printing” originated from the act of a central bank literally printing new banknotes to hand out to people directly to spend, with no payment-in-kind. This is the most basic form of inflationary currency debasement, with the most famous examples of it from the Weimar Republic and Zimbabwe.

All forms of money printing, including the modern types, must share some characteristics with the basic form.

To do so, they must follow these two rules:

“Printing” must create negative equity at the central bank, otherwise it is considered to be sterilised;

The money created must be spendable in the real economy OR it facilitates the creation of more debt that creates more spendable money.

QE fails on both points, as it doesn’t result in negative equity, and doesn’t create money that can be spent in the real economy.

Overpaying on bank reserves relative to what is being earned on the bond portfolio is a form of money printing. Negative equity is created, and can’t be reversed. The extra payments to the Fed’s counterparties will eventually be realised as reserves fall, and will result in greater profits that will end up in the real economy.

Cancelling debt seems to fail on the second rule. While it definitely creates negative equity, it doesn’t create any spendable cash, being an accounting entry only. To be inflationary, the government would have to use that extra borrowing capacity to expand debt at a faster pace they were before the cancellation event. Since this is similar to giving a man a new banknote and expecting him to spend it, we will pass debt cancellation on both measures.

If the government doesn’t change its behaviour, then this is equivalent to printing banknotes and giving them to people that destroy it and don’t spend it. Money printing that has an inflationary effect (the only type we should care about) might not just be about the central bank, after all.

There is an unanswered question in what would happen to the bank reserves created during QE to amass the bonds that would be cancelled. Two possible theories:

1. They remain, unable to be called on forever. The Bank of Japan continues to create money to pay interest on reserves. This would amount to additional money printing.

2. They are cancelled, and the banks would have to be recapitalised by the government. This would have the same effect as just conducting QT, and would eliminate the effect of debt cancellation.

I have a question: Agree that QE is NOT money printing. But what would happen if the Fed stopped paying Interest On Reserves (IOR)? Isn’t IOR the only thing keeping banks from doing “something” with the excess reserves to earn a return (ie make new loans, buy securities, etc)? Would that be inflationary?

Just got around to reading this, thanks Peter. We are facing a (kind of) similar situation in Argentina, where inflation has currently reached 100% YoY, and the CB has net income losses, reaching a point where increasing the benchmark rate only leads to higher inflation. Highly unlikely the US reaches that point though.