The non-stop rally in the Nasdaq and S&P500 this month has been one of the most amazing things I’ve ever seen in macro markets.

Everyone is saying it’s confidence. It’s an overheating economy! Yet real retail sales have been stalling for months now.

It’s not even the magnitude of the rally I have an issue with. 13% happens quite frequently especially after a large drawdown. It’s the unbroken spell that took us well beyond prior all-time highs without a second thought. All without a resolution to what could be one of the biggest energy crunches in history. Apparently, all that’s needed is the concept of a resolution.

There are two explanations for how this happened.

The “war is obviously over” argument and negotiations will just work themselves out;

The downside case is so obviously catastrophic that any reasonable trader was positioned defensively and a massive short-cover ensued, coupled with a US obsessed global market in which the US is least affected by the closure.

I favour #2, in line with my “binary markets” theory. I firmly believe this ridiculous reaction is purely because participants can’t really process what is just ahead of us down the road, so they are desperate to seek safety in the herd. And the herd was buying. This isn’t driven by confidence, it’s driven by fear.

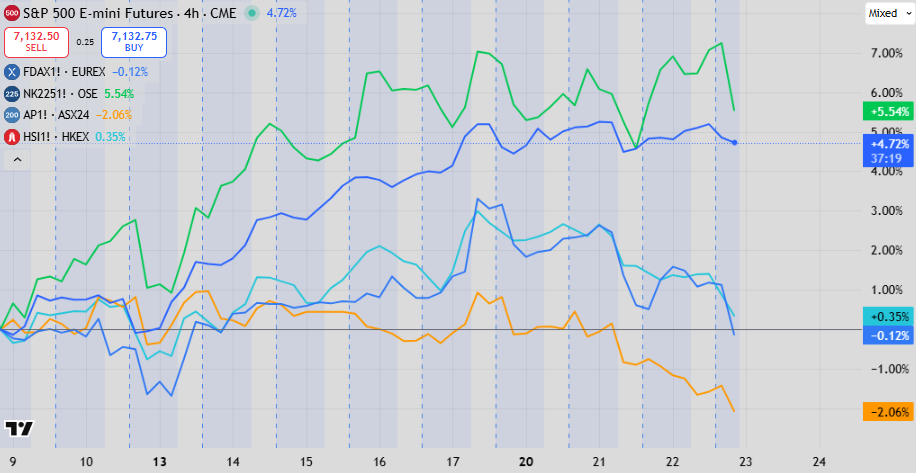

We need to look cross-market to confirm. The post “ceasefire day” gap breakout rally has been limited to the US and Japan. Few markets have participated, and the closer a market is to the fuel crisis, the worse that markets performance has been.

Australia is the closest to rationing, with diesel and jet fuel reserves hovering between 20 and 30 days, with lack of any visibility of deliveries in May. Australia has very little (~20%) domestic refining capacity, and also nearly all of its crude oil production is sent for export.

The performance here has been stark versus the US, underperforming heavily since “ceasefire day”. I expect this to continue.

The prospect of fuel rationing hasn’t been the only thing causing this underperformance. Fuel prices have already made their way into some pretty serious inflation in construction materials and at the supermarket. Delivery costs are up 30-50% which flows through to nearly everything. Home-brand milk has been marked up by 12% at one of the large national supermarket chains.

This is coming for you no matter where you are.

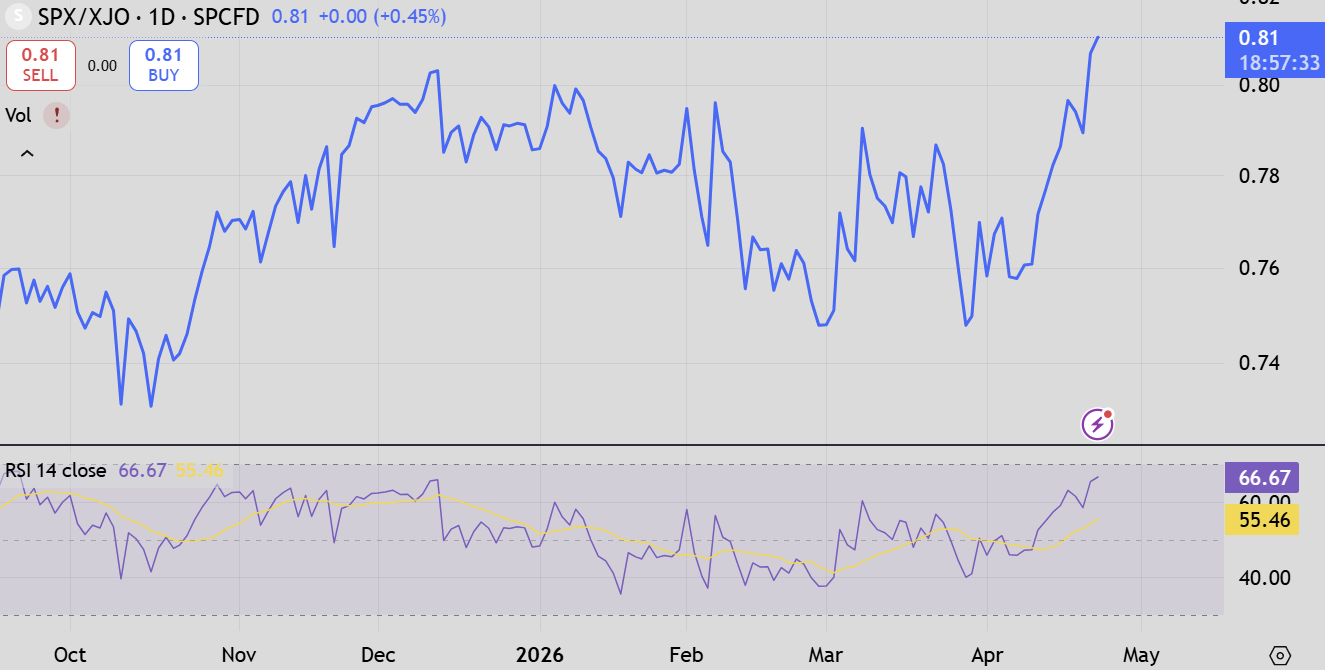

Australian equities were the first to fill the ceasefire gap.

The fact remains that Australia (and Europe which has seen a similar level of underperformance in the chart above) is already experiencing the effects of a closed Hormuz. Every day that passes will see this ratio head north, until one day when the US starts feeling the effects. This will happen within equity reporting (remember the S&P500 has about a 40% revenue exposure to foreign markets) rather than fuel effects directly, which will take longer.

We aren’t there at all when it comes to recognition by US markets. And this allows it to get carried away with the “Mythos” trade which is one of the frothiest things I’ve ever heard. Can Anthropic even deliver on compute which it’s already been struggling with? Didn’t we all hate AI because of the huge capex spend in the 4 months before the war? We all like it again now? OK, sure.

Has anybody even seen and used Mythos or is it the equivalent of “Gabbo is coming” from the classic episode of The Simpsons?

The fact remains that everywhere apart from the US is not convinced “war is over”. Even if it was, there would still be some probability priced in that it wasn’t. All-time highs are one indication that downside isn’t priced, as is the vol crunch.

Vol doesn’t make sense

Front-month VIX futures didn’t trade over 30 and we got the bounce we did. It seems that markets front ran itself here - many look at this level as a key point to start buying.

The VIX itself is at 19 against realised volatility of about 13%. This is a lower premium than what persisted for most of February and March.

Implied volatility prints well above realised when fear of the future encourages downside hedge buying at a greater rate than current volatility would suggest.

This lines up with the persistently high put buying that I have spoken about for the last 3 months, which has now sharply turned to call buying.

Market structure has changed because of the use of options, especially in the US. Highly protected markets find it difficult to go down as dealer hedge buying overwhelms. This leads to the “stairs down, elevator up” pattern that is upside down from what has persisted in the past.

Rates need a discussion

Large downward moves in US equities are difficult to conceive after what happened in April. Rates markets haven’t bought the recovery in the same way that equities have. This point casts further doubt on the validity of the rally as well.

Inflation at this point is a certainty. How central banks deal with it is going to be the next question.

For the ECB, repeating Trichet’s mistake of 2007 might well be on their minds. The ECB however has a more explicit mandate that is tied to inflation.

6-7% headline inflation is baked in at this point. It can be worse of course. But if the supply side shock hurts growth more, will central banks change tact? It is a possibility.

Being short rates seems to be the obvious trade here, but I’ll have to leave a deeper dive on that until next week.

In the meantime, keep an eye on Dec-2026 /CL future. It seems to have attracted liquidity away from the broken front-month contract. The chart above shows little evidence that the “war is over”, and in fact highlights how prolonged this crisis will be.

Panic rallies usually look mysterious only if liquidity is ignored.

When yields stabilize and financial conditions stop tightening, positioning unwinds fast.

Systematic exposure rebuilds.

Risk parity re-leverages.

Vol-control adds back equity beta.

Price often moves before the narrative catches up.

The real question is whether liquidity is confirming the move or just allowing it temporarily.

Odd that the currencies of the countries most exposed have largely been strong - AUD has continued to trend up.