The more time passes, the more it seems that Iran is a headless chicken running around with a drone/ballistic missile/ASCM strapped to its back.

Iran’s actions are making less sense, making them seem more desperate than being in a position of control. But the fog of war is thick.

This isn’t to say that the headless chicken can’t inflict huge damage and disruption. They currently are by firing indiscriminately on commercial ships and infrastructure and attempting to mine the Strait for no other reason than to create chaos as it is their only bargaining chip left.

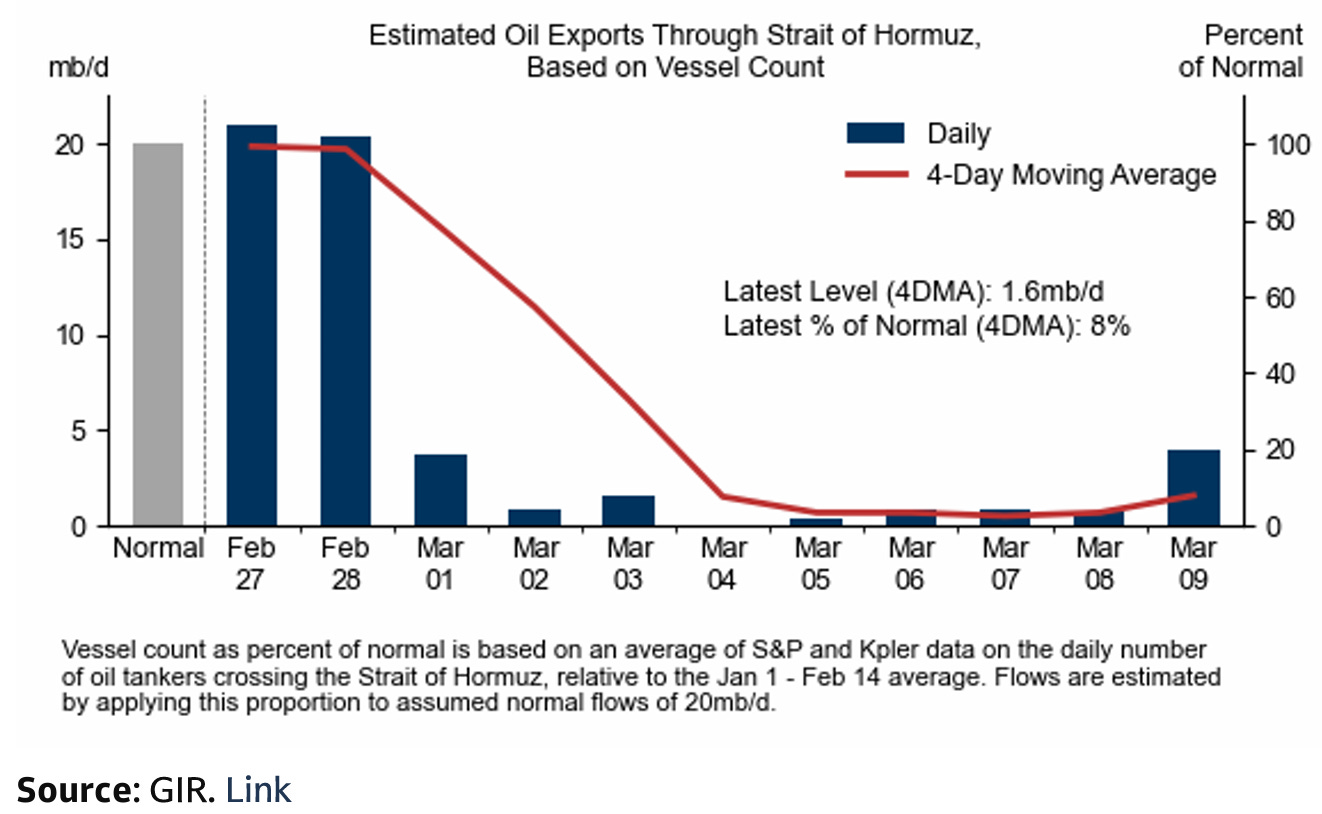

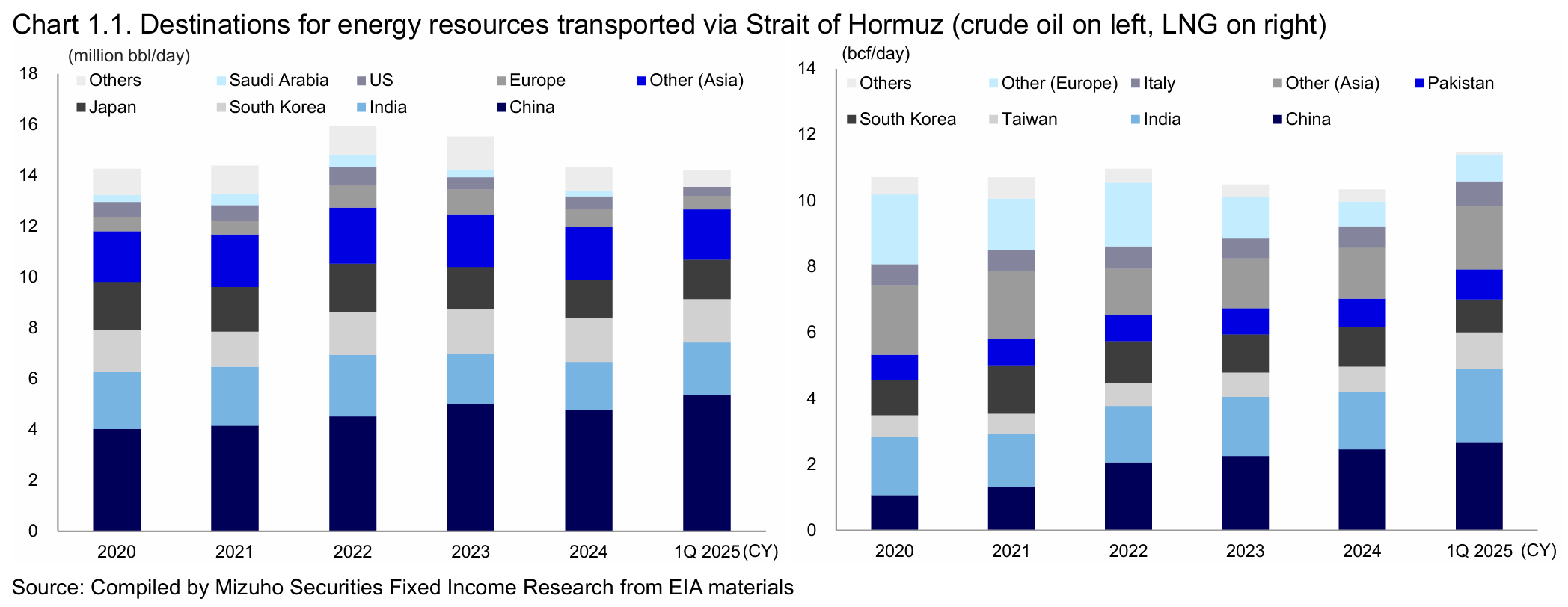

There may have been a chance that they had a friend in China by allowing Iranian tankers to traverse the Strait (those in the chart above purported to be heading to China). Goldman (perhaps as an attempt to validate last week’s heavily panned view) were the only ones to capture the movement of these vessels.

These situations have shown China to be extremely transactional in its approach to alliances, and this one is no different. In this case it would still be problematic for China in that it was used to receiving 4-5mbpd through the Strait before the war. It is unlikely to be held at that level.

Then there are other questions related to non-US aligned oil getting through the Strait. Iran has fired on Chinese flagged ships and has also declared it was going to lay mines in the Strait.

Lay mines and nobody gets through, not even Chinese oil on Iranian tankers. Smart mines, guided navigation? Probably not, although who knows. If it does close the Strait entirely then this crushes Iran’s own financial capability.

Shooting oneself in one’s foot is not always evidence of stupidity, but rather desperation. The question is whether desperation is weakness, or their power.

Either way the truth remains that a full closure of the Strait will be economic devastation for the world, and very few will be immune, even if energy self-sufficient.

And it’s not the crude oil I’m worried about. It’s the urea, LNG and helium supply that are impossible to divert and are even more important than oil in maintaining a functioning global economy as we know it. Disrupting urea means disrupting fertilizer production and means stunted food production. Expensive/non-available food production equals civil unrest.

The possible outcomes are so dire that if the US Navy can’t find a way to ensure relatively safe passage, then the US will just have to give up and pull out. The other outcome is just not feasible when it is avoidable. If they don’t open the Strait after that…well we’re in for trouble.

When you are getting too negative about the conflict it is worth keeping this in the back of your mind. The stakes are high and responses will have to adjust to this reality.

Nobody, even Iran, is interested in a Strait that’s closed. But a headless chicken is only interested in running about aimlessly, and they can do this for longer than you would think when it comes to defenceless shipping and infrastructure.

In the end it’s not that much of a different feeling to trading through the GFC or the pandemic. Be realistic about the bad outcomes but also realise there are actions that can be taken that may result in them not happening.

Equities

Divergences are closing in the relative performance of markets.

The underperformance by “short energy” countries occurred mostly in the first few days of the conflict.

After that point, the divergence is minimal at less than 2%. The US outperformed during Monday’s big drawdown but also recovered less. The short-term trend is fairly clear here.

Many are surprised by this sort of slow burn sell-off in equity indexes. To me it makes perfect sense. The extreme cases (US wins and gains control of the Strait or nobody gets urea/LNG/helium and dies) is so vast that we can only price in the middle. Individual headlines (another tanker gets attacked/a desalination plant explodes) are negative, but these events singularly aren’t important in themselves, so no single event can cause a large drawdown. Many more tankers will get hit. Eventually the market will become immune to it (as sad as that sounds).

The US was the clear outperformer as everyone that needed to be hedged was hedged already and it was one of the few countries with energy independence.

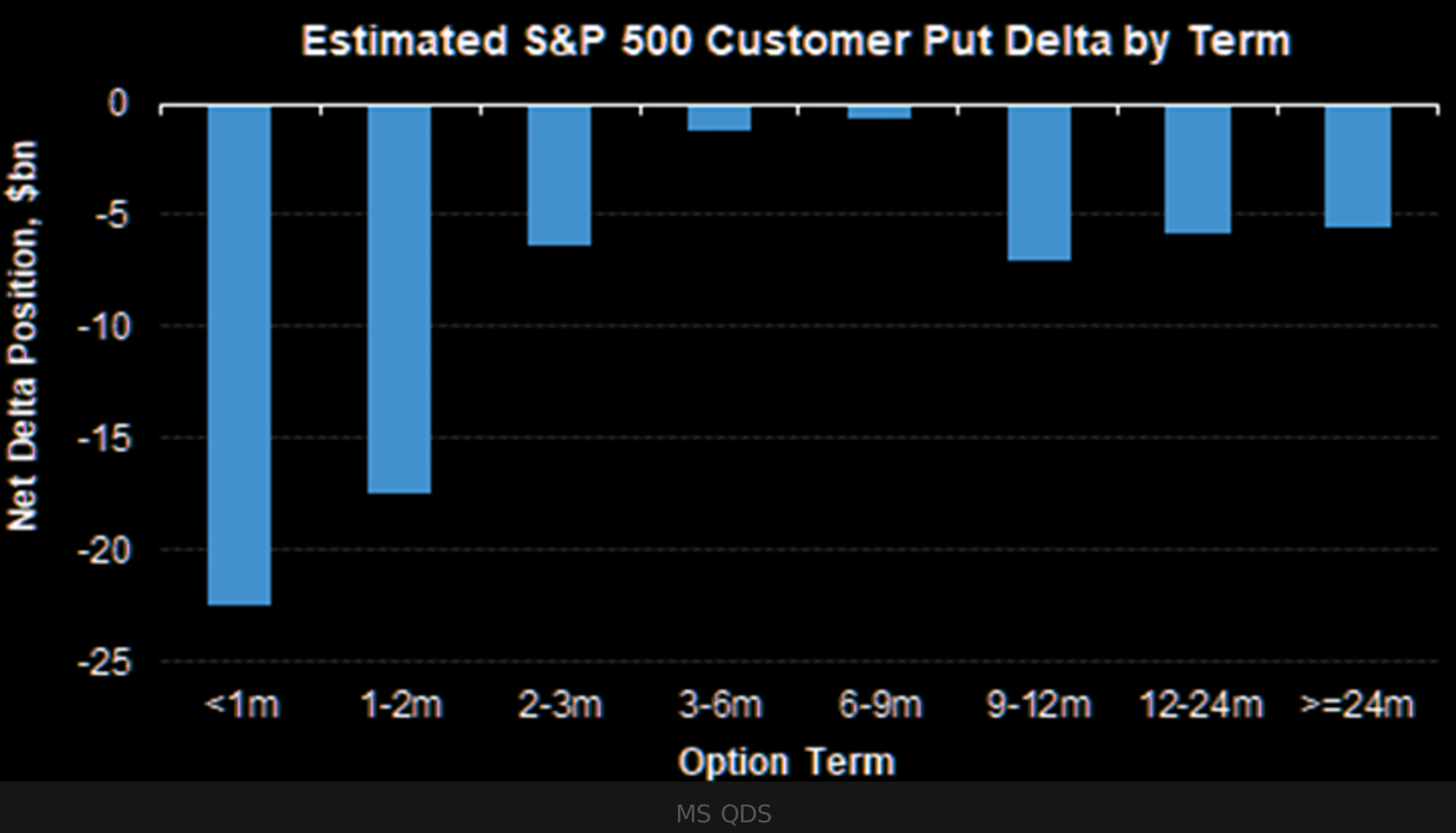

Keep in mind that hedges expire and must be replaced. Important if you believe the downside is capped. Having said that, a slow burn downwards will still likely make these hedges losing bets.

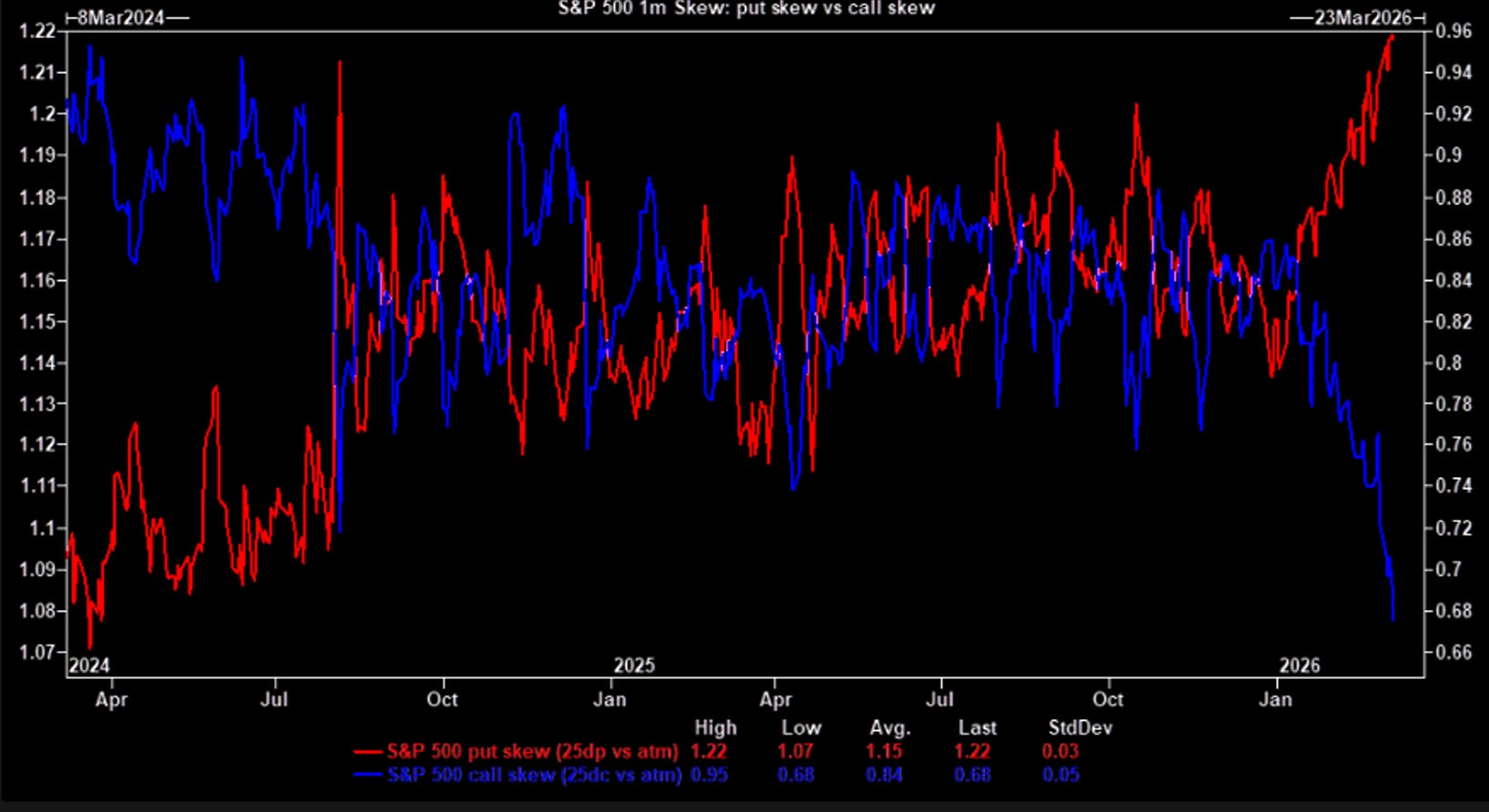

The skew isn’t lightening up for the those rolling hedges though. The move in equity markets for breakeven returns on these hedges is only increasing.

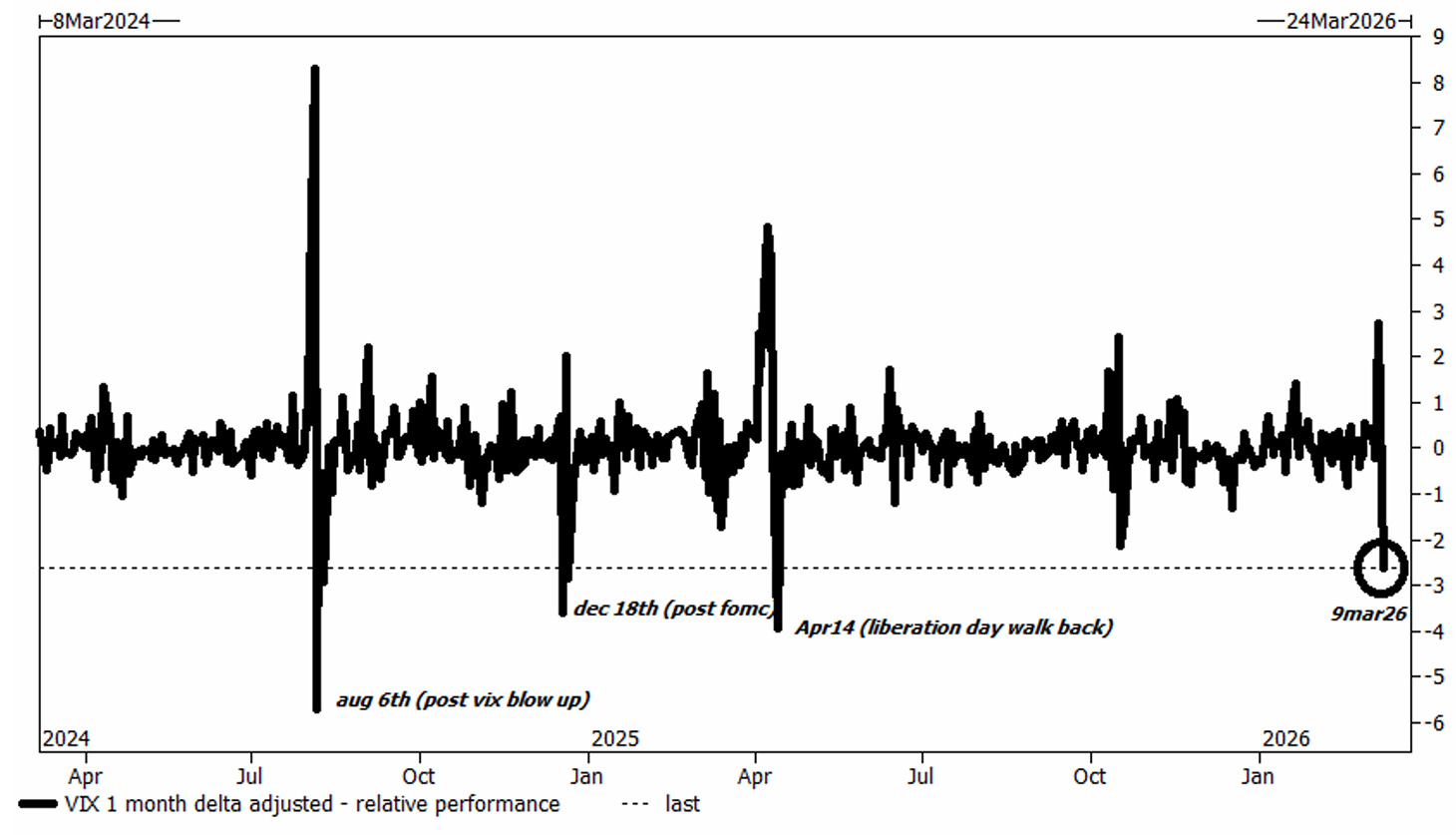

For another measure on how implied volatility pricing has outpaced realised see the chart above. VIX futures have underperformed by far more than delta has to been in the league of other vol market blowups.

Japan

Japan sold off heavily this week; however, this has tempered.

Increased confidence around the size and accessibility of Japanese oil reserves and source of their LNG has revived some confidence here.

Japan has huge sensitivity to the pricing of these commodities however, and it may bring back worries around another current account deficit situation with implied effects on the Yen. That cross is back in rate-check territory which freaked out markets in January.

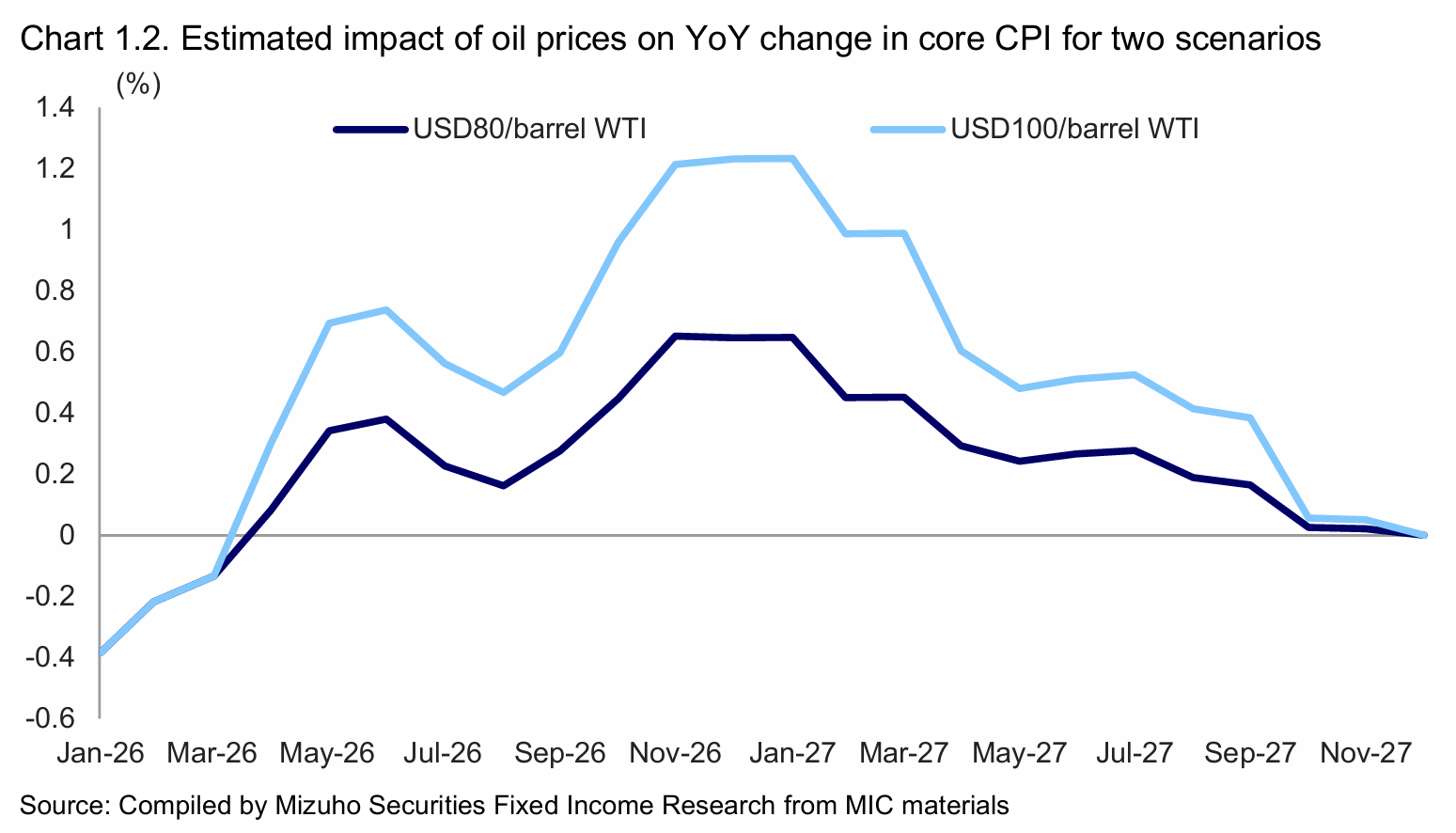

I’ve avoided commenting too much on inflation forecasts from the effect of skyrocketing oil prices because it’s slow and not the dominant effect moving markets right now. The above gives an idea to the hit on core CPI in Japan given different scenarios. A declining Yen will only exacerbate this.

In the midst of all of this, US February core CPI printed weak! Does anyone care? No.

Just ask the front end of European rates who have not only sold off ~70bp but have had to endure 30bp intra-day ranges. Brutal.