Tariffs that reshore must create inflation

Defining the "successful" tariff, featuring the tale of the washing machine and dryer combo

Will tariffs push up costs for US consumers and drive inflation higher? This seems to be the only question markets seem to care about, despite being entirely unrelated to whether the implementation of tariffs is a success or a failure.

The inflation question is an easy one to answer as we’ve been through tariffs before in the first Trump presidency, and I will use one of the early examples of tariffs to walk through what happened and why.

The spoiler is that the 2018 washing machine tariffs did cause inflation for a period and thus were “bad” by the market’s definition, but the ultimate answer is much more complex.

The complexity arises on what the definition of “success” is when implementing tariffs. Inflation is the focus of the market, but Trump clearly has other goals which include reshoring of industrial capacity and the social benefits that flow from that.

I’ve always had a more positive view of the use of tariffs in such a tactical manner by the US as their global consumption heft gives them a strong negotiating position. The US is essentially using its position as the world’s consumer to exploit the adage that when you are big enough, “the customer is always right”. The size advantage doesn’t guarantee success; however, it does make it more likely.

The market’s question posed above, while important in understanding the reaction of the Fed, misses the point when it comes to the topic of tariffs. The most interesting part is analysing why tariffs were both a success and a failure for Trump’s extended goals.

It will become clear that tariffs that are trying to rebalance global trade must weigh up the price signal of tariff driven inflation that relocates capacity and the reality of competitive advantages between nations. Changes can’t happen without that price signal, so tariffs that don’t create inflation likely won’t work to balance trade.

Our learnings from the humble washing machine

Searching Google for “the effect of 2018 Trump tariffs” reveals nothing but a bunch of partisan fearmongering from either media outlets or politically aligned think-tanks. Each article will have an ounce of truth within it but knowing what is and isn’t true and what has been omitted from reporting is almost impossible. Why it is such a divisive issue is lost on me – the Biden admin kept most Chinese tariffs and increased them in specific sectors. The facts are that it is bipartisan yet getting information on the subject seems like it isn’t.

So, we are going to have to look at this ourselves.

The last trade war officially started in January 2018 with tariffs on washing machines and solar panels. Once the ball was rolling, tariffs strengthened the US Dollar against nearly everything (including the Yuan, below).

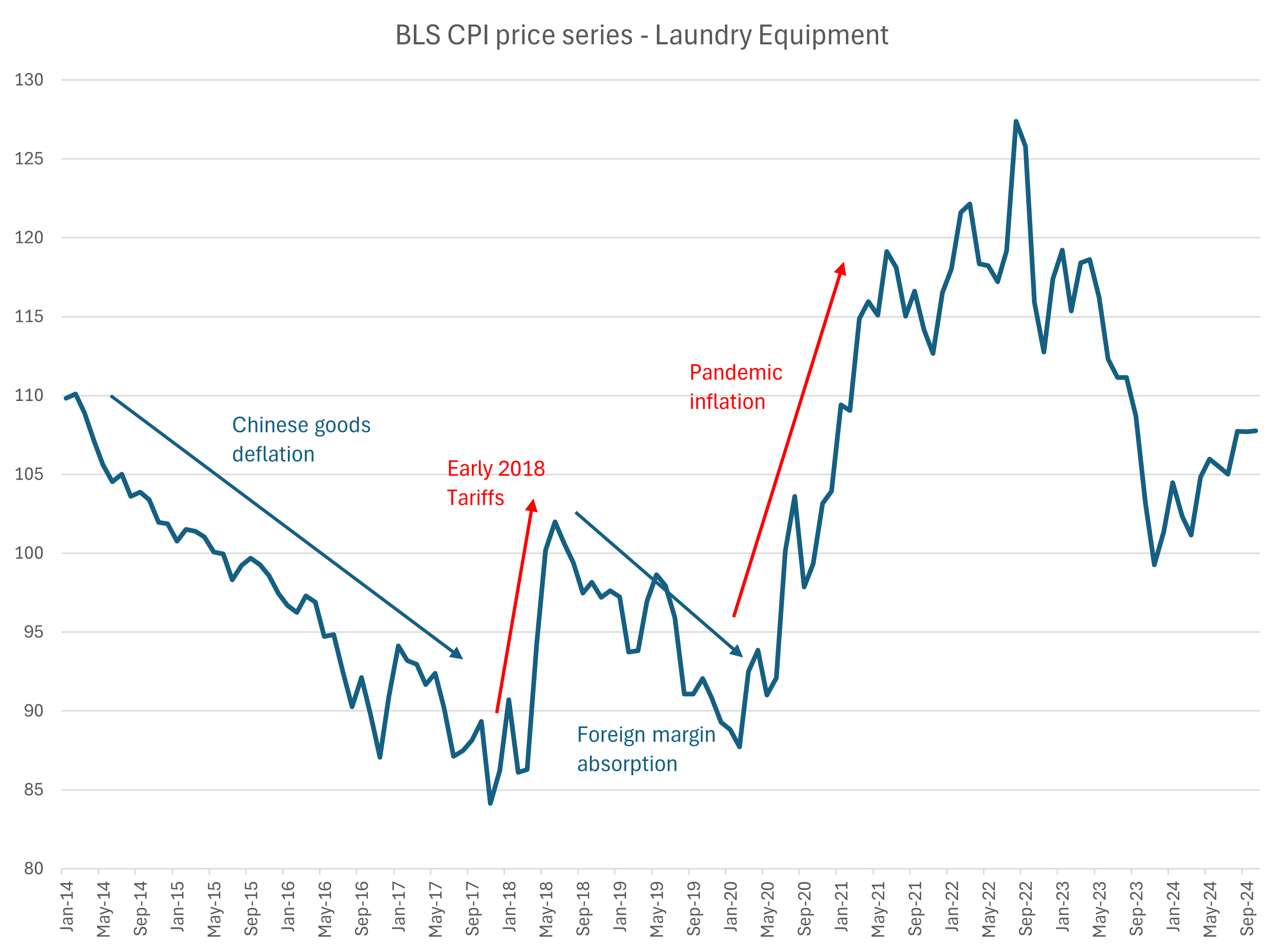

The implementation of tariffs well before the pandemic means we have multiple years of data and their subsequent effects on pricing. I’ve chosen washing machines as an example to illustrate what happened to prices over the period. The data is presented below.

Tariffs announced on washing machines were 20% for the first 1.2 million units imported, and then 50% after that (originating from any country). The 20% tariff can be seen directly in the CPI series, with a 1 for 1 translation visible.

If you put “what happened with the 2018 tariffs” into Google the articles that want to paint tariffs as universally “bad” (because they caused inflation) will stop their analysis here. However, this spike in prices was short-lived and prices eventually fell back to their original levels over the next 2 years.

This paper from the NBER uses data to the end of 2018 to estimate the effect of tariffs on prices and they get to an answer of 12%, like the BLS data series in the chart above.

You may notice that I am using the BLS data series pertaining to “laundry equipment” rather than washing machines. This is because the price of dryers also went up by the same magnitude around the time of the tariffs being applied despite not being subject to tariffs. This is possibly due to manufacturers trying to reclaim margin on both items as they are commonly bought as a set. Either way, it is more indicative to include all related items in this analysis and despite this by the end of 2019 prices had fallen back to original levels.

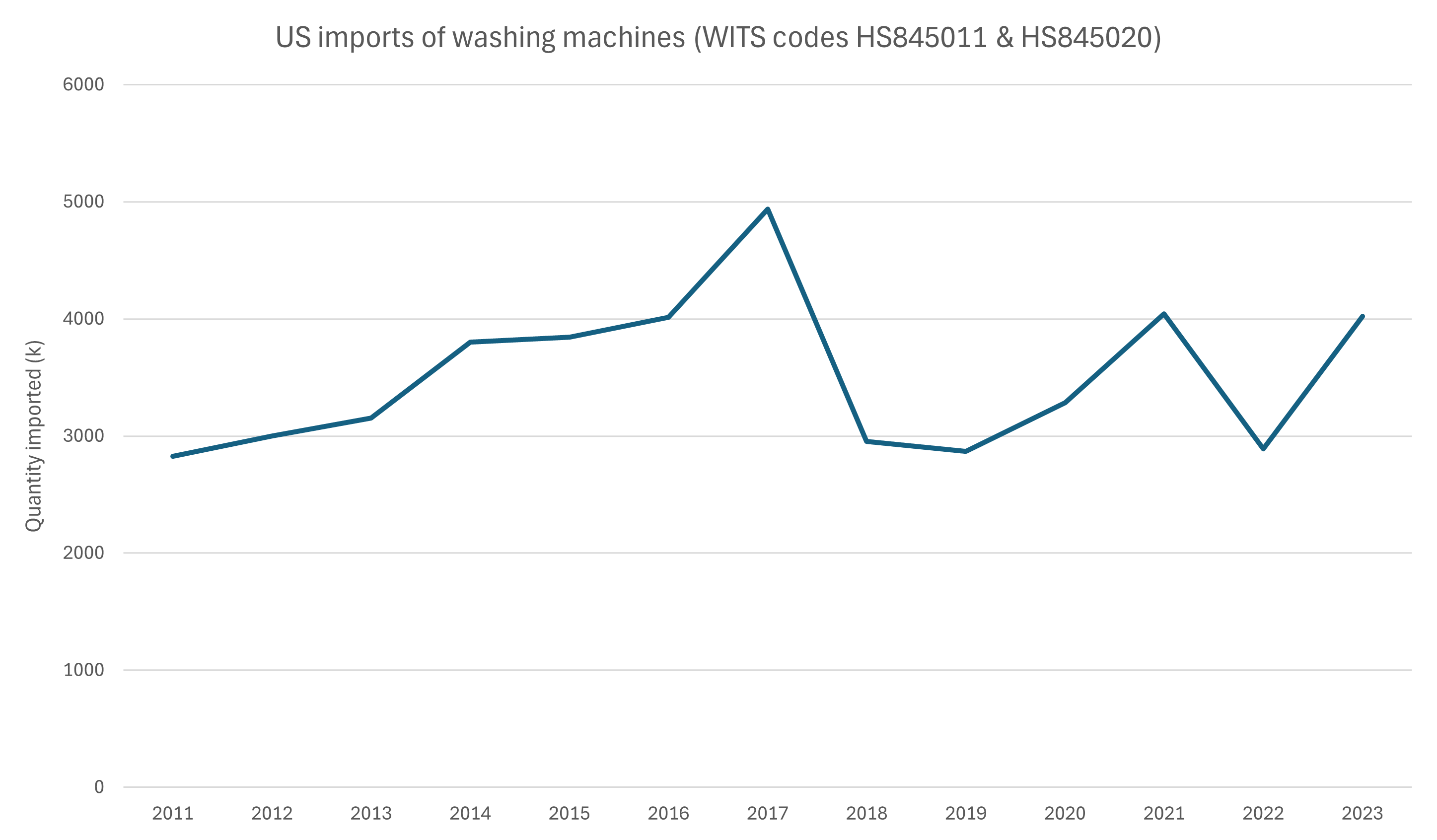

In this example it is also helpful that China was also not the source for the manufactured good either. July 2016 anti-dumping laws against China were initiated to relate specifically to washing machines. This resulted in Chinese manufacturing capacity shifting to Thai, Vietnamese and Korean manufacturers and made actual Chinese sourced washing machines far from the major target of Trump’s tariffs. This can be seen in the chart below as imports from China (the red line) collapsed as the anti-dumping laws were introduced.

The pre-tariff surge in total imports (the purple line above), led to imports falling considerably after their implementation. Once these stabilised however, imports by volume stayed lower than before the anti-dumping laws were implemented.

As imports resumed, a new lower equilibrium was found at about 1 million units below the 2014-2016 average.

A major reason for this permanent fall in imports was due to companies relocating their production into the US. Two examples are Samsung moving production to South Carolina, and LG to Tennessee.

It is only in the most recent 2023 data that the quantity of washing machine imports has picked up again, however it is worth nothing that the US had grown roughly 19% in real terms since the end of 2016, implying that domestic production had in fact made up for more than the absolute level of imports has reported.

Given this data, we can say that:

Protectionist measures didn’t lift absolute prices on washing machines in the medium term; and

Protectionist measures increased domestic production and stopped import growth.

This varied by the type of product tariffs were applied to. This example merely shows that the blanket conclusion that tariffs will result in inflation and don’t work to reshore manufacturing is false.

Volume vs Price

If volume doesn’t change then neither can trade imbalances. Price is needed to get a value comparison, sure, but volume is what is manufactured and created in the real world.

On this measure washing machine tariffs were a success where the China specific anti-dumping legislation failed. The anti-dumping legislation just moved production out of the targeted country, where tariffs had moved production back to the US.

If this is the case, does price matter at all?

Price and quality (more specifically higher price and worse quality) are usually associated with tariffs and other forms of trade protection, because of their association with their use in the 70s and 80s. Free trade brought cheaper and better goods, where countries enjoying a competitive advantage on expertise, raw materials or labour cost could out-compete local manufacturers.

By stopping manufacturing relocating to those countries, consumers paid for those jobs or investment to continue locally through higher prices and lesser utility. This is a real cost that amounts to a subsidy of those industries.

So, did the US consumer pay for those jobs to be relocated back to the US? This is a harder question to answer.

On the face of it by the end of 2019 those washing machines and dryers cost no more than they did before tariffs were placed on them, meaning that no, there was no cost.

However, a valid argument that can be made is that these goods perhaps would’ve been 20% cheaper than where they ended the experiment if tariffs weren’t applied, but we cannot say that with certainty. Without access to the counterfactual, we could just as easily say that prices may have been higher. While unlikely, we just don’t know.

We can say with some certainty that foreign producers absorbed some of the tariff into their margins. This is an important point, and highlights both the circumstances that allow tariffs to work this time because of the important role that the US plays in global trade in perpetuating the huge imbalances that persist.

Why tariffs will (selectively) work for Trump

The US is the world's consumer and has been for the last 45 years.

The US has accounted for more than 50% of the world’s total trade deficit since Japan emerged as an export powerhouse in the 1980s, and only gave up this role for a brief period in the early 1990s as the effects of the Plaza Accord allowed the US to regain its footing as an exporter at the cost of Japan (and nobody was there to take the title of leading mercantilist economy after the Japanese bust).

The same was repeated as China rose, with the US reaching a peak of consuming 73% of the world’s net trade in 2003.

The dip in the early 2010s were due to weak Dollar policy and the shale revolution which reduced oil imports and switched the US over to an oil exporter, helping to mitigate the deficit. This was only short-lived.

Since then, the US’ share has generally stayed in the range of 50-60% on the world’s total trade deficit.

If you want the reason for why the US can hope to benefit from applying tariffs on imports, it is simply this. Like any business, if you have one very large client, they own the ability to set the terms. If what you provide isn’t unique enough, then the customer has the power to set their own price.

You might be thinking that tariffs aren’t a negotiation on price as they just get slapped onto the top of the good’s price and there is no change for the exporter. This is where the buying power of the US becomes important.

If the exporter allows the tariff to increase the landed price of their product, there will be a hit to volume. Since the US is such a big consumer, there is no other way to make up that volume elsewhere.

If the US is 60% of global imports, then how will you make up that fall in volume anywhere else? It would be incredibly difficult, if impossible.

So, to keep volumes up, the manufacturer will end up choosing to absorb some of that margin or employ other techniques to reduce the cost price of manufacture. This is precisely what we saw in the washing machine example above. The consumer eventually saw no price increase, the US government received their tariff, and a considerable amount of production was relocated back to the US.

An Earth-sized version of “the customer is always right”.

The size of the customer (importer) in this relationship turns the relationship of importer and exporter on its head.

My view is that China is more reliant on the US as a destination for its industrial capacity than the US has demand for goods that it can’t fulfil with its own industrial capacity. Understanding this is key to predicting all retaliatory moves by each side.

Small countries don’t play by the same rules because they can’t replace the industrial capacity. It also doesn’t work in examples where the export country’s offering is unique and can’t be relocated elsewhere. This is an example of true competitive advantage.

We know that washing machine production didn’t exhibit uniqueness because production was quickly relocated to Korea and Thailand after anti-dumping laws took effect. This made it a good candidate for tariffs.

When it comes to goods with these characteristics, applying tariffs has a high chance of success (when it is the US applying them). At worst they’ll generate extra revenue for the government, at best they may result in production relocated back onshore. Even better, they may be able to force a broader trade negotiation to level the playing field.

Successful in isolation

In this case, tariffs aren’t as bad as the economics textbooks would like you to believe, but it has been anything but a full-blown success. President Biden’s administration kept most of Trump’s tariffs, but net imports has continued to climb, albeit at a slower pace than you would expect.

China has managed to grow its trade balance in goods significantly since 2019, relying on export markets outside of the US.

Trade in goods with the US is higher but has underperformed real GDP growth and is also pandemic affected. You can also see this in the US’ share of total world deficits – since the end of 2019 it has fallen slightly from 65% to 55% or so.

Where negotiations will go

Trump is a deals guy. He understands the advantageous position that the US is in, and the reliance China has on the US as a market, and he knows the pressure tariffs put China under, even if there can be some friendly fire on some groups at home.

By using this leverage, he can guide China towards a negotiation, and this negotiation could take many forms.

Recent rumblings from Chinese leaders about an intention to devalue the Chinese Yuan are surprisingly showing the Chinese hand a little early.

There is little reason the Chinese would genuinely need to devalue their currency at this point. Exports are still growing quickly, and they are most definitely aware of the upset this is causing. Even the Europeans are talking about protectionism which shows how dire the situation is there.

A devaluation of the Yuan would bring with it outward capital flow pressure, and for a year where foreign direct investment contracted again and is back to 2012 levels, that likely isn’t a step they would take to put further pressure on a weak economy.

While I wasn’t the one to coin the term, a “Mar-a-Lago Accord”, in similar vein to the Plaza Accord of 1985, would be a suitable resolution to the question of tariffs. The agreed upward valuation of the Yuan would have to be hefty to get a deal done – the figure would be at least 20% higher over a period of a few years.

We saw what happened to the Japanese external balance, and subsequently their economy, when the Plaza Accord was agreed to in the 1980s. The Chinese have surely learnt from this and will surely be careful when negotiating. At some point however tariffs may be a preferred alternative than an across the board decrease in competitiveness from a much higher currency.

What is Trump’s goal?

A critique of tariffs I’ve read more than a few times weigh the possible benefits of returning manufacturing to the forgotten parts of America will possibly be offset by a net increase in prices of goods that these same people consume.

The use of tariffs will only be effective towards this goal in the case where tariffs are offsetting subsidies in the competing country, so that the tariff is not trying to forcefully offset a genuine competitive advantage.

Sometimes it will cost to reshore, but this may bring other benefits. Reshoring can promote gainful employment especially in small communities where the value provided by the relocation of capacity is greater than the cost of reduced consumption due to more expensive goods.

This is a contentious point, especially as we emerge from the inflation of the last 3 or 4 years. MAGA also seems to want to accept this trade-off, but as always, we’ll need to see how it turns out in practice.

Take this all too far and it may turn out to be policy that protects uncompetitive industry and is bad for everyone in the long run, as this alternate form of subsidy encourages inefficient manufacturing and lacklustre innovation.

This leads us to the ultimate point about tariffs. If you believe that China is practicing with an effective unfair advantage either through:

A managed currency;

Cheap state sponsored debt;

Allocation of resources to the supply side of the economy; or

Highly divergent environmental and labour regulations

Then protection makes sense to promote domestic industry and try to reverse some of the social ills and the political upheaval that have come along with its decay.

If you are doubtful of these unnatural advantages, then you must ask why trade imbalances have only become worse and not better? Theory suggests that trade imbalances can only persist for a short period of time as market pricing should account for any for cheaper inputs, and only true natural advantages should persist.

Are tariffs the best solution to the problem? Probably not, but they are far from the worst solution and a continuation of the status quo is untenable for the reasons outlined above.

While it’s impossible to know Trump’s true intentions with regards to tariffs, my best guess is that they will once again be used as a blunt negotiating tool to try and reduce the tilt in the game board that China has had in a serious form since 2008, with an increase in its severity in 2015.

As a tool for negotiation Trump can hope to achieve a goal that is somewhere in the middle of the extremes.

One extreme is the totally reshoring of global manufacturing capacity to the US. It is unlikely that this is plausible or in the US’ best interests primarily due to the cost and feasibility of manufacture.

The other extreme is that tariffs are only to raise some revenue for the Federal government and as such don’t lift inflation at all.

The real goal might lie somewhere in between – the acceptance of some inflation and reduced consumption for some reshoring of industrial capacity. If this is the goal, it will be apparent in the goods that are chosen for tariffs and what negotiating terms are accepted. Right now, we can only guess.

The washing machine example was an example of an outcome between the two extremes. Some capacity was reshored, while the bulk was still imported.

The irony

The goal of moving industrial capacity back to the US can only happen when there is a price signal that forces it. This is true for all changes in a capitalist system.

That price signal is the increase in the cost of imports, which will flow through to US inflation. This, again, is a certainty.

Limited change can occur without a price signal by, let’s say, sternly convincing foreign companies that it is their best interests to reshore production. This effect works, but only in certain circumstances.

Trump’s tariffs haven’t fixed the trade imbalance between China and the US. This we know.

The key learning is that this fact also has meant that Trump’s tariffs haven’t lifted prices meaningfully enough to affect inflation, and this makes the definition of what is a successful tariff a tricky one.

If they’re successful because they didn’t drive up inflation, they were also unsuccessful in their effect on reshoring in any meaningful sense.

If you deem them to be unsuccessful this time around because they drive up inflation, well then, they’re more likely to succeed to bring the US trade deficit down.

Very few in the political sphere seem to be able to discern between the two definitions.

In the meantime, keep an eye on the US Dollar. January’s rally has captured the reality of tariffs, and while the rally has been faster than back in 2018, we still could have a few percent more to go.

Great write up, thanks 👍