This week’s viral AI piece highlights more about level of uncertainty about the payoff from the exponential growth in spending on AI compute rather than the eventual effect of it if it does succeed. Capex intentions over the next 3 years by the biggest megacap tech companies will total the entirety of Australia’s GDP. How could this not be a huge source of uncertainty in itself?

On an annualised basis it competes with some of the biggest investment programmes of all time. This time around a lot of that spend will end up reflected in the drag from net imports in GDP, as a lot of the metal isn’t produced in the US. The infrastructure and meaningful expansion in the supply of electricity will, however.

From my point of view the uncertainty of whether AI will work on a cost-to-benefit perspective (and thus offer a return on capital) is the bigger question than what it will do to employment or the regular person’s welfare in 5 years’ time.

The economy is an infinitely complex system, and respect must be given that nobody knows how individual actors will respond given such an incredible change to how we work if AI is successful in delivering intelligence at a cost that is far less than labour. And that’s a big if.

If the capex does produce viable cost-effective intelligence, will there be another whole sector of employment that arises from this? Who could’ve foreseen the rise in the “bullshit email job” as a result of industrialisation that so many lament and criticise as a driver of poor productivity growth now? Who is to say the infrastructure spend doesn’t just drive a new commoditised market in inference? What if AI drives a return of the more dynamic and higher productivity small business that can compete with large corporates without breaking a sweat? This outcome alone would be incredible for the economy.

The effect on AI on much white-collar work is no different to mechanisation and then automation through robotics of much factory work on blue-collar workers, but both of these developments just resulted in more and higher quality consumption. The offshoring of what remained of manufacturing in the US after this surely had a bigger effect than the automation itself. Offshoring itself is a result of other new technologies like the commercial aircraft, better shipping and the internet - technologies that have delivered many more benefits than drawbacks.

In preparing for this piece, I struggled to identify new widely adopted technologies that didn’t ultimately lift our standard of living, even if they had other downsides. Even something horrible like asbestos provided significant benefits in the reduction of deaths by fire before the true downsides of that discovery became apparent (and then hid by many companies for many years). Social media is another. The benefits probably outweigh the drawbacks even if the drawbacks seem more corrosive.

If you can think of any widely adopted technologies that only caused downsides, please drop them in the comments.

I don’t have the answer for what will happen, but all I know is that AI is becoming a more useful tool as it develops and has found some real uses in my own daily workflow. Whether it will remain cost effective after subsidies end, I’m not sure.

The development of new technology is the only way to expand productivity and lift the standard of living. If it doesn’t do that, then it likely won’t be implemented and it will fail. We’ve been through the “there is better and cheaper labour somewhere else” cycle a number of times and it always seems to work out. There are losers, and there are winners, and the economy (and politics) reshapes around this new reality.

Being negative on a new technology that is years from viability also strikes me as negative when the default option should be optimism.

A possible failure and thus nervousness about the capex spend coupled with the real downsides to some business models if it was successful is really what is driving markets right now.

Tariff decision, yet no vol respite

I was wrong on two counts last week. The SCOTUS decision on IEEPA tariffs came before the state of the union address, and its announcement didn’t really take the vol premium out of markets, even if equity markets are trading higher than we were on Friday.

With the decision out of the way (which at this point doesn’t have much effect one way or the other since they will likely be implemented in a different form), it only leaves the continuing dispersion and volatility of the constituents of the S&P500 as the culprit.

Despite Thursday’s session seeing a mild sell-off at the index level, dispersion has started to decrease.

Until dispersion lowers, index level volatility can’t decrease, and the persistent buying of put protection likely won’t slow.

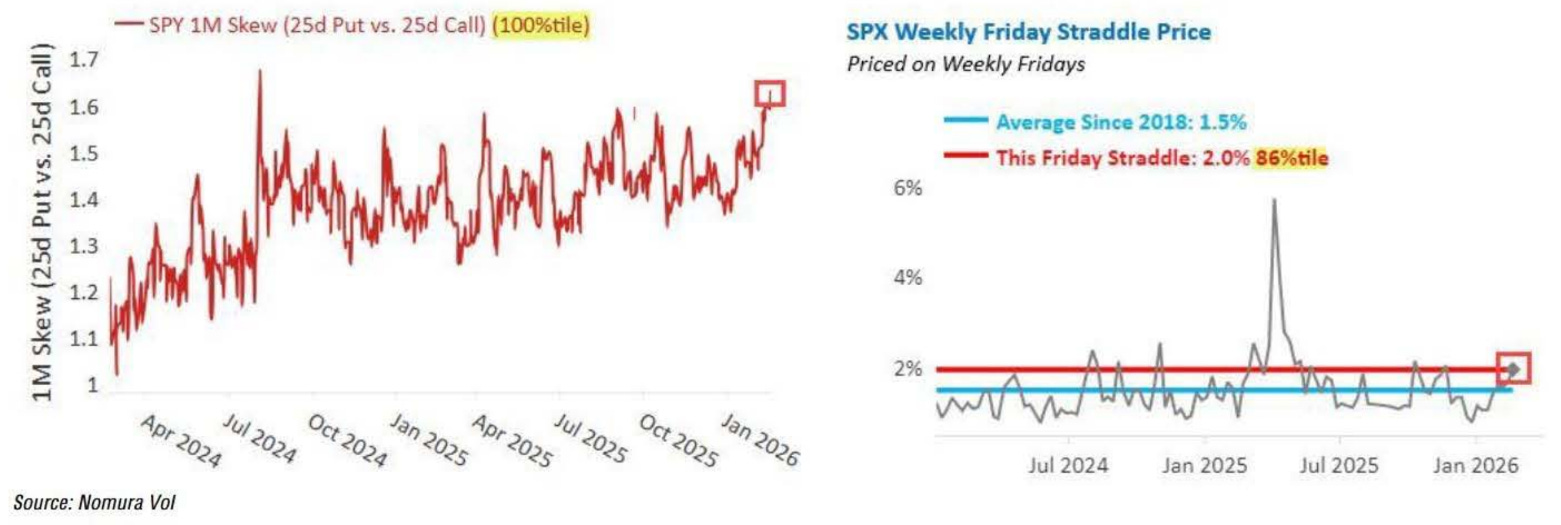

The volatility skew and straddle pricing remains elevated…

…and the first VIX future has failed to break lower.

Dispersion can however moderate in a number of ways, with all stocks starting to fall a possible solution to that problem. This would likely require a rout in semis.

I’ve written about this a few times now, but these dynamics are key to why the US market continues to struggle relatively. While European markets haven’t done a huge amount better over February, Korea and Japan have shown that there is still considerable appetite for risk. It’s just not anywhere near the big tech spenders.

To look at this market you need to put your credit PM’s cap on. A credit PM (who maybe owns Microsoft or Oracle debt) will be looking at skyrocketing capex plans and reevaluating their exposure both in size and where it is bucketed in their portfolios.

CDS spreads have widened from ~20bp levels in 2024 (much safer than most of the index) to about 40-50bp now, (Oracle is in the 120’s). This is still lower than the average in the IG index, but this repricing will directly carry through to both equity volatility for each name and their P/E premium, as illustrated in the chart above. Their businesses have meaningfully changed and the market needs time to digest that. The nature of “tech” has changed.

Does 40-50bp seem tight given that a number of these firms are in a capex war? I would argue that it does, especially since a number of these companies no longer generate much (if any) free cash flow now after capex. The wider spreads go, the higher implied equity volatility will be, along with lower multiples.

Rates follow-up

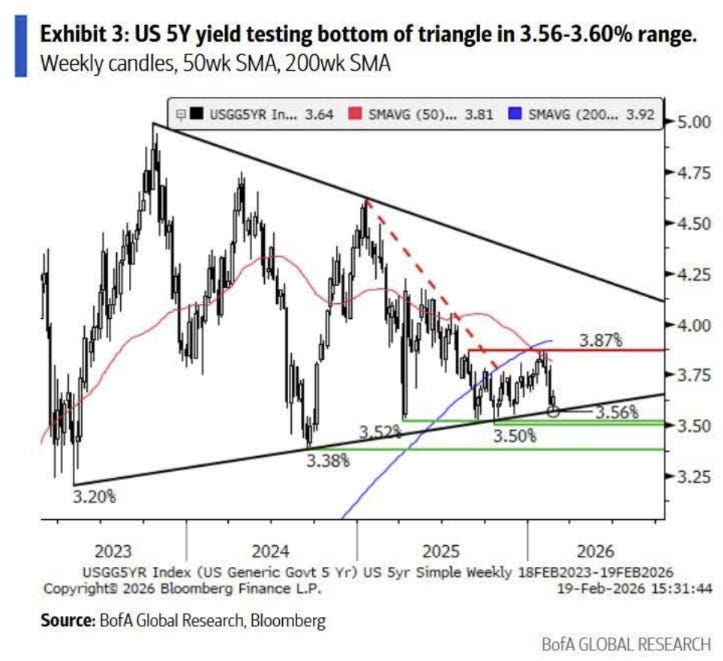

Dec-2026/Dec-2027 SOFR is now starting to price cuts after last week’s move extends.

The belly continues to outperform…

…but it’s likely to hit some resistance.

European bonds continue to do well which is surely dragging down yields in the US as well.

China requires some attention

Missing from narratives at the moment are movements in China. The USD just can’t catch a bid, this is no less apparent in USDCNY, which is usually a low volatility managed currency.

The RMB has appreciated continually since liberation day, to the tune of about 6.2%.

Keep in mind that this is the nominal exchange rate. Anaemic inflation in China versus the rest of the world has meant that it is still as low as it has been despite the recent turnaround.

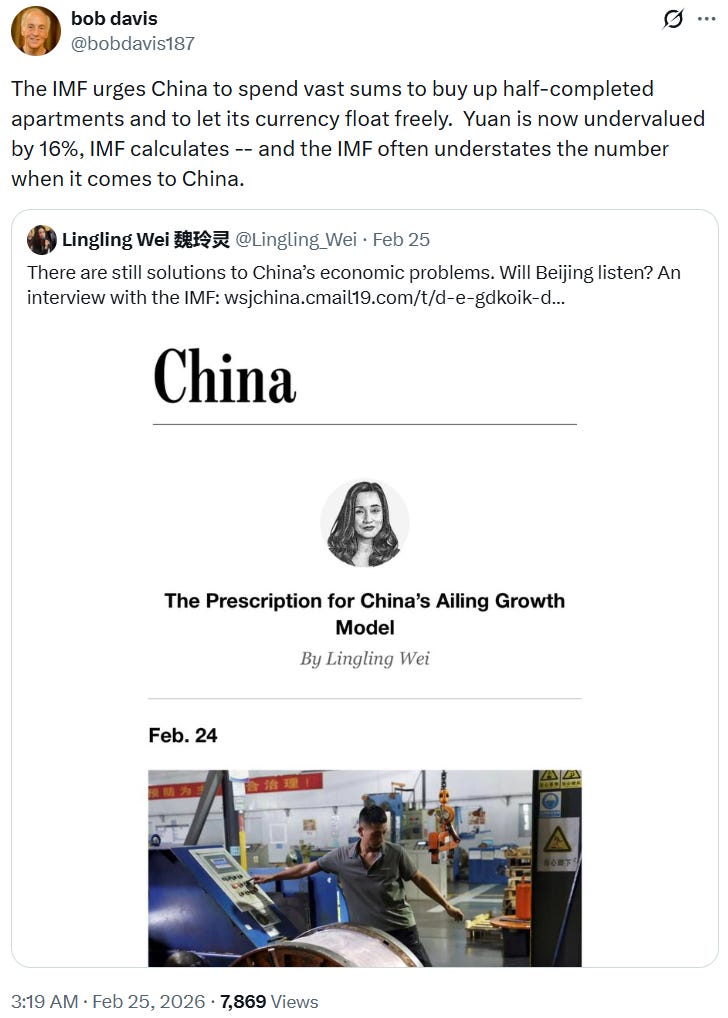

Even the IMF is recommending that China do something about it. This may have been prompted by discontent in Europe where even they are talking about tariffs. Either way their estimate of 16% undervaluation is likely way off the mark.

This article from late last year covers the dynamics well. They estimate the Yuan undervaluation is about 30%. More recently China seems to be acting against the move by directing state banks to buy USD to offset the appreciation, working entirely against the narrative that China is trying to “dump” US Treasuries.

While the economics are strong all across the western world, China’s is not looking good.

Net exports continue to prop up a continuing capitulation across the property sector.

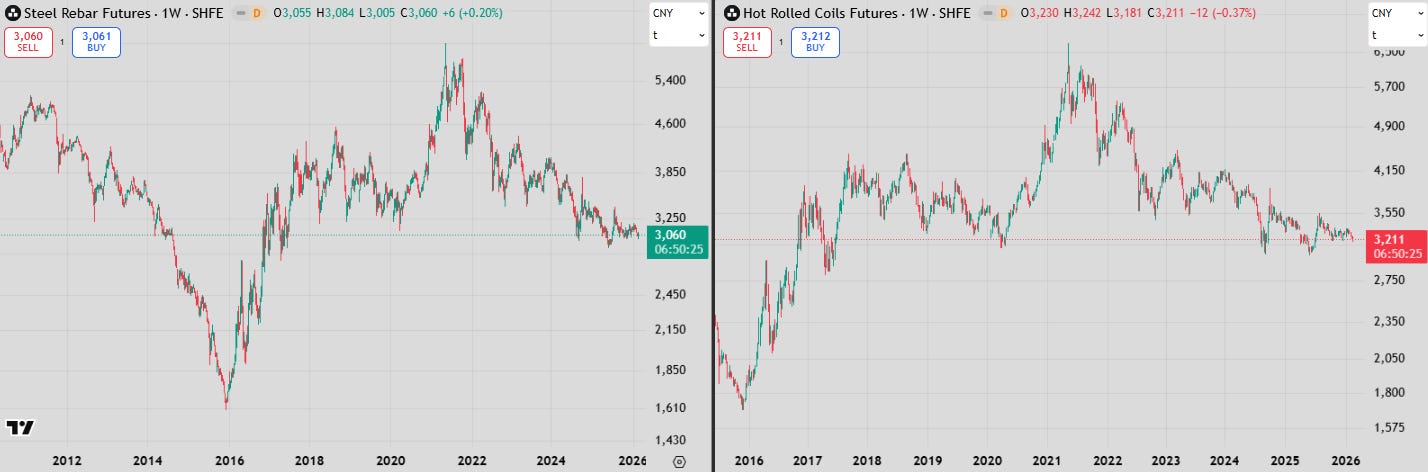

Steel pricing isn’t showing any signs of life but isn’t necessarily breaking down either.

Leaning against the currency doesn’t seem like great messaging about the state of the Chinese economy to me. A lot wrong with the world now would correct if the RMB did appreciate, but China’s reliance on net exports as the only engine of growth will ensure that this doesn’t happen.

I struggle to see how the Yuan can appreciate against the USD for roughly 40 out of the last 50ish sessions without the chinese government active participation given their monetary policy.