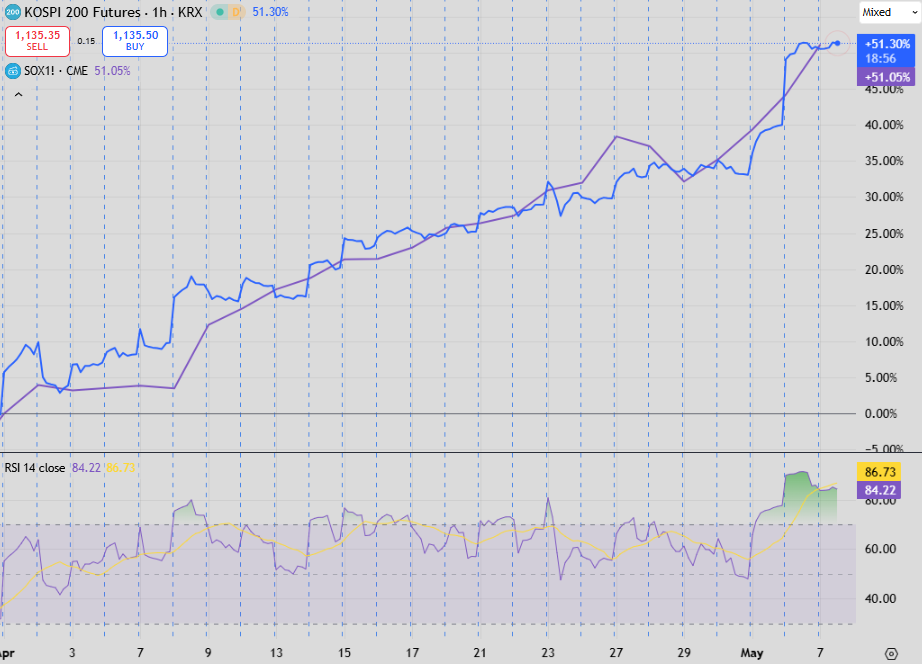

The panic rally in equities continues.

What started (and continues) as a parabolic move in semiconductors is now pulling up stocks that are more directly affected by energy disruptions. Health markers for this rally are poor, but you would expect that when it is so concentrated.

What we’re seeing now is just the acceleration of the “infinite demand at any price” theme that has dominated since 2020.

I could post any number of bear fuel charts whether it is based on breadth, volume, number of stocks hitting 52-week lows etc. There’s no point as the narrative is unlikely to be broken now.

The rally has gone on for long enough now that even impaired markets are starting to get dragged along.

Europe was interesting this week. The nadir in underperformance this week versus semiconductor exposed markets happened on a night of heavy company reporting. Reports were good enough to spur a decent rally, but how the market is choosing to interpret results is indicative.

Germany’s BASF, the biggest chemical company in the world, reported on April 30. BASF is front-and-centre when it comes to Hormuz disruptions, with feedstock for its various chemical processes doubling or tripling in price. Feedstocks along with LPG and jet fuel are most affected by the crisis.

The company said that it increased prices across segments affected by 30-40%. Did such a large pricing bump negatively affect company guidance? No. BASF kept 2026 guidance at the same level as before the crisis.

Analysts reacted by either holding or upgrading BASF. It is now trading well above where it started the year, roughly in line with the pre-war price. The general consensus was that there was room for margin expansion given the current environment. Raising prices gives you more pricing power the more you hike, apparently.

There is clearly another way the market could have taken these price increases. Huge price increases (with possibly more coming) would be bad for demand so they would affect both margins and volumes. There are few historical comparisons for these sorts of spot increases, so you would expect some disagreement amongst analysts about their effect. That isn’t the case.

You can’t bet on demand contractions

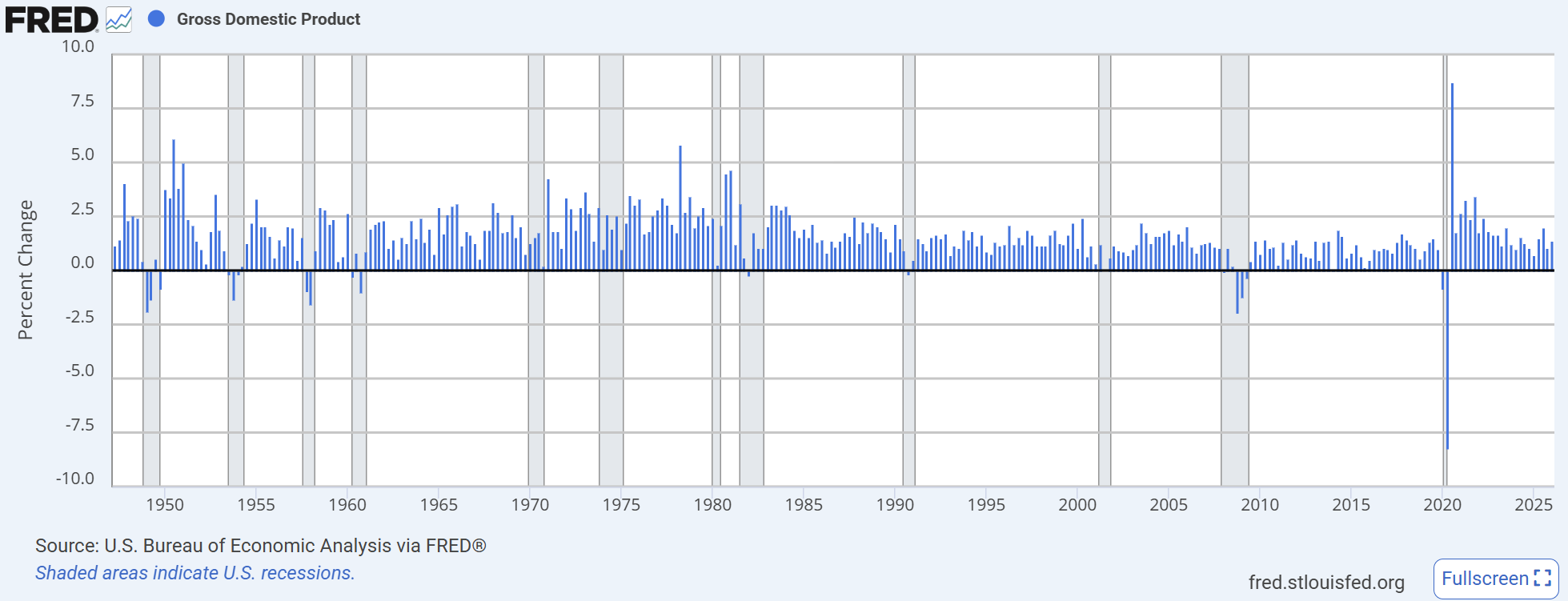

This newsletter is called Macro Is Dead because the business cycle - a natural contraction in demand that encouraged natural destruction of capital - just doesn’t exist anymore.

If you had bet on a contraction in demand during the pandemic for anything longer than a month you got your face ripped off by the market as governments deployed unlimited firepower to hand money to people that weren’t allowed to produce anything. This ensured demand didn’t contract (with the ultimate effect being inflation due to that supply side contraction).

Demand was held buoyant while the supply side contracted. This meant that the only cycle was in inflation rather than on the demand side through a business cycle contraction. To the extent that GDP did contract it was for a an impossibly short period which violently reversed and led to a sustained boom after the fact.

In addition to this, the pandemic wasn’t a natural contraction in demand. It was manufactured by government through lockdown enforcement. That was a choice, for right or wrong. The “recovery” was similarly manufactured.

This means we haven’t seen a natural contraction in demand since 2008. It follows that you would’ve have to have been in markets for more than 20 years to know what such a process looks like and what it’s like living through it. Generally, sell-side analysts aren’t that old (it’s always been a young person’s game to grind for those hours and to get constantly berated by your underperforming clients).

Forecasting demand contraction means putting a “sell” rating on a stock. Who would put a sell rating on a stock in this market? Long/short managers are hardly bothering with the short side of the book anymore! Who, as an analyst, are you selling to if nobody will short anything anyway?

How the market views BASF extrapolates to everything else we are seeing. Broad macro is unaffected as near-term GDP forecasts remain strong and recession probabilities low (although in the US for good reason, I explain below). Applying the same idea to the AI/semiconductor complex explains plenty if you are confused by it.

Infinite demand for compute

Calling the rise in AI-related stock prices a bubble is just wrong. P/Es are very reasonable. As many have said, if there is a bubble it’s in E rather that P.

I would argue calling the even the “E” part as a bubble is contentious. If you subscribe to the “infinite demand at any price” for AI, then it’s all absolutely reasonable.

You don’t need that much to happen to justify everything we’re seeing.

All new compute capacity has to approach 100% utilisation. If it does, then hyperscaler margins will be realised and all of the hardware (chips, memory, power delivery etc) would be a great investment. Great margins for all. Ignore the accounting argument about capitalisation of costs. The cashflow will certainly arrive.

The LLM companies can continue to attract capital to run at a loss, are able to push pricing to break even, or can engineer a jump in efficiency.

It’s just another version of the “infinite demand at any price” coupled with the endless supply of capital. Demand for inference will stay high enough that both capacity will be filled and pricing will eventually be able to adjust.

This is why calling it a bubble might not be appropriate. There very well could be incredible demand as the technology progresses.

This is still a panic rally though. There really isn’t much that’s healthy about this price action. SOX is up 50% this month with no pullbacks. Everyone wants to buy on a pullback. This means it won’t happen.

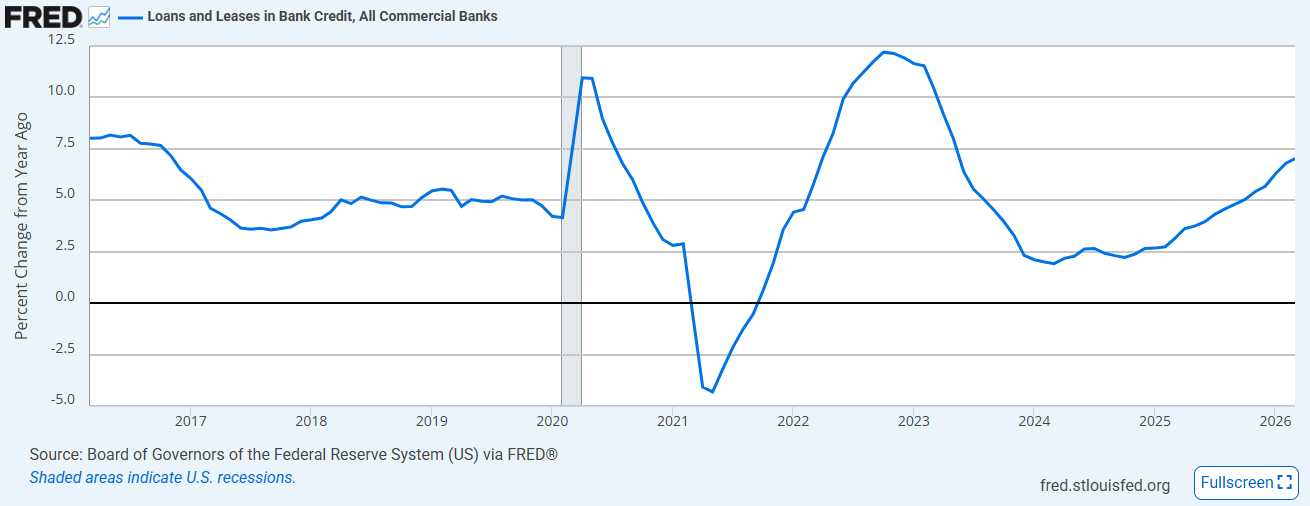

There is a very positive read through on hyperscaler capex that is a genuine bullish macro story. Since free cash flow has been consumed by investment, debt will become a more important part of funding these projects (it already is very important but will become more so). The economy is manufacturing more capital.

Bank lending has exploded in the US. This is a very important determinant of GDP growth and equities strength.

The almost certain bull case for US growth

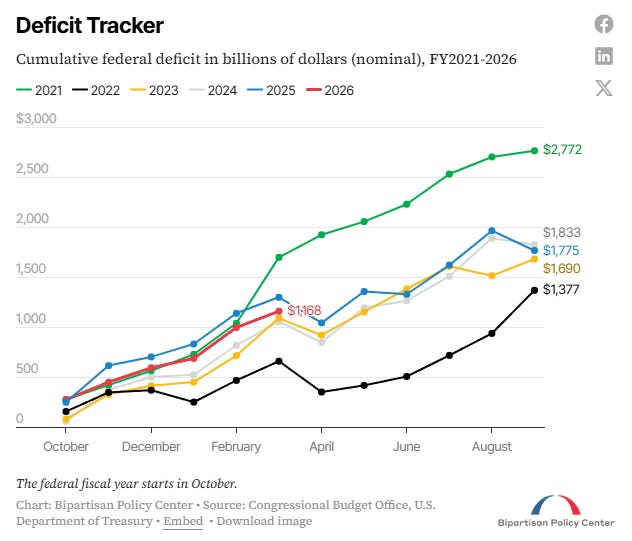

My last newsletter drew out the linkages between domestic debt accumulation and GDP growth. It’s time to put those conclusions to the test.

If you want to read about sensitivities on this, the newsletter above explains how fiscal and bank debt growth are the primary factors driving both. Note that fiscal is growing as well, right in line with other very bullish years.

Looking forward where it suits

The trade in equities is all about looking forward with optimism and applying the lessons learnt over the last 5 years when forecasting demand.

The trade in oil and macro is no different. For the supply issues in oil, you really only need to consider the chart below for why the market is happy to accept the current status quo.

Total crude and product liftings are back to where they were before the war started. How? It isn’t because of a magical resumption of Middle Eastern supply. It’s because of a huge uplift in exports out of the US.

This isn’t being met with new supply. It is draining from inventories which has an obvious maximum shelf life. Drawdowns of onshore US inventories break records every week.

You don’t need to be Nostradamus to know that this can’t go on indefinitely. Inventories are already below what they normally are for this time of year and reflect the lowest they have been in the last 5 years.

There is no free lunch here. Inventory draws also put pressure on US product pricing even with crude <$100. Gasoline futures above illustrate that.

On the other hand, surging exports are another reason you’ll see a great GDP print for the next quarter even if some of this is gets detracted from negative inventories.

Supply has been bolstered by inventories, but at the same time oil analysts have been pushing out their dates for operational stress in commercial inventories. Asia and Europe to be hit first, but probably somewhere in early June as opposed to May. Another reason for the bid to risk.

Despite this, the market’s bias here is clear.

Demand is unable to contract looking forward when it comes to corporate profitability.

Supply in oil that is unable to contract because of where things are at the present. And if that fails, demand for oil that is able to contract if supplies do become an issue.

One looks forward. The other doesn’t. Why? Because you are the clown if you bet on stock prices falling. Cognitive bias will adjust to get to this outcome.

Thanks for this post, I largely agree in the intermediate term. Three risks come to mind with the AI trade: 1. Hyperscalers and private equity are like the Fed with QE, price insensitive buyers. However unlike the Fed these sources of capital cannot print money. So you can be price insensitive up to a point. Will that slow earnings momentum and start a price reversal? 2. How much are the hyperscalers/PE subsidizing AI demand? How much would Anthropic need to raise prices to generate the ROI needed to justify this level of investment? Sure at these prices AI demand is infinite because it’s basically free. Model efficiency is key here and I haven’t heard much about this yet. 3. Supply bottlenecks. This ties into 1., but prices are spiraling for everything AI related. Heavy construction and electrical equipment firms are trading at 30 forward PEs. Is there a point where hyperscalers admit their buildout ambitions are severely hindered by lack of supply and costs?

Especially liked the BASF anecdote. Thanks for putting this together