Contradictory "data-dependent forward guidance" is out. Great!

Charts & Notes: Week 24, 2026

Kevin Warsh hosted his first press conference as Chair of the Federal Reserve this week and we’re all in for some changes.

We already knew that he wasn’t a fan of forward guidance. This is music to my ears, and it should also be for any rates trader.

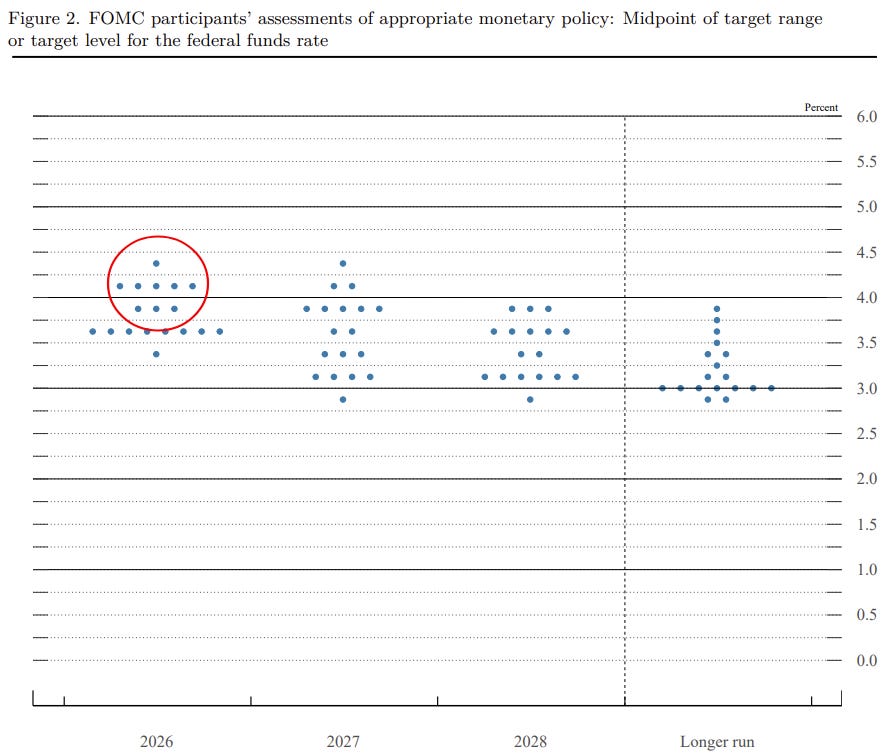

The dot plot is likely dead with the end of forward guidance as well. Good riddance. The dot plot never made any sense because it was in direct contradiction with the Fed’s quarterly economic projections and their stated goals.

How could you possibly have upward long-term revisions to forecasts for the unemployment rate or inflation if the stated goal of your forward “dots” is intended to manage both of these things lower? I don’t think they intend to make their own monetary policy seem ineffective, but I don’t see how you can’t come to this conclusion.

Forward guidance and the dot plot are remnants of being at the zero lower bound (ZLB) in rates throughout the 2010s. Since rates where at zero and the Fed were already buying bonds, pinning the belly of the curve required aggressive use of forward guidance to ensure the market never started thinking about anything resembling a rate hike.

The other benefit of this was that it drastically reduced volatility in rates markets. Less volatility in rates markets transmits to higher valuations in risk markets, another direct intention of the full-court press style monetary accommodation.

Then came the pandemic and a Fed slow to act in combatting the inflation that was generated from that event. The “dot plot” or forward guidance here were absolutely useless and possibly held back a market from adjusting to reality when it needed to for the purposes of sending the right pricing signals.

Warsh himself was likely the member who didn’t submit their dot to the plot, and that sends a clear message.

The dot plot itself was the reasoning given to fairly brutal sell-off in rates post conference, but I’m not sure that is the right answer. More on pricing later.

Along with the attitude toward forward guidance is a far reduced post-meeting statement that looks ridiculous when applying a difference filter.

The less words, the better. Now we just need to ban Fed board member speeches, and we will truly be free!

The obvious implication (and trade) is for structurally higher rates volatility. Absent a shock, rates should ebb and flow more with how economic data changes than being pinned around what the Fed’s forecasts of the overnight rate is going to be. The market’s assessment of the medium-term path for Fed Funds should trade is a greater range than previously.

Rates positions need to get smaller with this new Fed.

To add to this, Warsh expressed the view that the Fed shouldn’t tell the market how they will even react at all to data! Warsh, from the press conference Q&A:

I think financial markets perform best when they react to incoming data. I think the financial markets work less efficiently when they ask a question, how will the Federal Reserve react to that incoming information. The more that markets are paying attention to what’s happening in the real economy, deciding what’s good data and what’s less good data, the more financial markets can price what they believe is the most likely and what are the tail risks.

Financial market prices are probably the most important source of information to guide central bankers. But when all the financial markets are doing is reflecting back what we’ve said, we’re taking the most important source of information and we’re being blind to it. I’d like us to create a system where those blinders come off, where markets are following data that they efficiently think is reliable and they’ll be watching data, we’ll be watching data.

They’ll come with better information through market prices to us. We can make more informed decisions. Ultimately, the goal I set at the outset, deliver on the price stability objective that Congress told us to do, and that we’ve got to get in the business of doing.

I get the idea of what he’s saying, and the “management of our data-dependent forward guidance” obviously went way too far with endless statements and hedging of those statements through multiple channels. Not only defining the reaction function but also telling you the output of that reaction function.

This all sounds great, but the Fed still sets interest rates! Ultimately every player at every point on the yield curve is interested in what the next move in rates will be. The reaction function still matters.

Perhaps Warsh wants the market to do it’s tightening for it by lifting 3-year+ yields. I know one guy who won’t be particularly happy with this!

For that matter, it’s tough to see how higher rates volatility works in this political environment either. So, while we might dream of having more volatility and a market that moves more with the data, it won’t take long for the Fed to be pressured to rein things in. Once again, you get to the point where a reaction function is found, and forward guidance starts creeping back in.

The first test came with the market move as a result of Warsh’s first go.

The first test

This might be controversial, but I don’t think the move in rates highlights a view that fits on the dovish/hawkish spectrum.

Markets almost immediately priced in near-term hikes in a fairly dramatic fashion, reversing some fairly difficult trading in the lead up to the FOMC. It was roughly a 15bp move higher out to March next year.

The dot plot showed that half of the board expected at least 1 hike this year. In sticking with my opinion that this chart is useless this should’ve been abundantly clear from the many samples of inflation data we’ve had since the last dot plot was released. Of course, some members would switch to hikes. This can’t possibly be new information.

Add to this the staleness of the dots. Oil has fallen 23% in two weeks once capitulation became clear. This will surely change opinions.

Maybe it was something Warsh said during the conference? He did stress the commitment to price stability a number of times. But what else was he meant to say? That he isn’t committed to price stability?

His focus on the number to the left of the decimal point was one of the more dovish aspects. This should give more space for inflation to run a bit, effectively moving the target from 2% to 2.9%.

The real answer probably lies in expectations. Assets sensitive to real yields falling performed well into the meeting. The consensus was that Warsh is a dove and positioning played into this.

Even gold managed to post a rally (a rare thing recently) into the meeting and then corrected fairly sharply.

Higher rates volatility also correlates with higher rates. Shrinking long positions after that press conference was the right thing to do, even if you still believe he will hold off hiking this year.

All-in-all, we just need to see how he plays out in the weeks ahead. We have gone back in time to a Greenspan era chair. There is no problem with this, but I’m unsure with populist politics it can remain like this.

THanks for sharing, Mr. Farac!

Great, as always.