Charts & Notes: Independence and Involution

Jackson Hole, Lisa Cook and China’s involution battle

Jackson Hole

Powell was more dovish, with reasoning given to the shift in employment trends.

Remember that central bankers tailor most of their communication for other central bankers, but when it comes down to it, they will travel the path that is most favourable politically to whoever is in power. It’s just never talked about so openly like it is now. Central bank policy is to minimise pain, and pain minimisation is popular at the polling place.

So, all you have to know is:

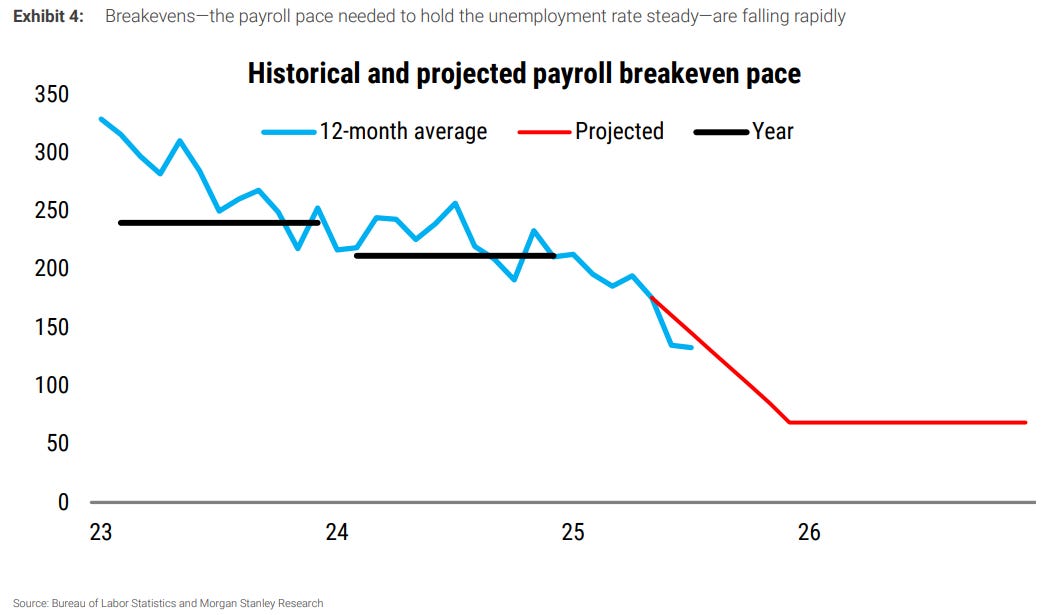

Slower working age population growth equals lower payrolls breakeven which increases the risk of a negative print. The modern central banker will drop all academic arguments in the face of employment faltering.

The Fed isn’t as concerned about inflation or the risks to inflation as they may talk about. If they did, they definitely would not have cut rates last year, when the outlook was for more uncertain.

The forward curve is pricing things fairly aggressively. It is totally consistent to not be an inflationista while being OK with being short the short-end of the US yield curve.

Adding to this, the nadir of the forward curve is at the lowest yield we’ve seen since the hiking cycle ended. This again is very tempting to short. While it is worth considering I don’t think it’s a great idea - there’s not a lot of gain in it and the risks are tilted against you, so maybe not as interesting as it first seems.

Stubbornly above-average inflation will continue to stress the long end of the curve as long as an easing bias is prevalent.

Lisa Cook and “Fed independence”

The Lisa Cook situation is interesting from so many angles.

The latest is that a lawsuit has been filed in which Ms Cook doesn’t deny any of the allegations around inconsistencies with her mortgage applications. At this time, she refuses to step down.

Questions swirl about the difference between being an employee of the Fed and being on the board of governors. While Trump may be able to remove her “for cause” from the board, it all leaves the Fed in an interesting situation with ending her employment altogether mainly because, well, they are the #1 financial regulator in the country, regulating things like how banks handle “mortgage fraud”.

Pulte’s move may be politically motivated, but it doesn’t change the facts surrounding any possible firing.

Deutsche Bank wrote on some less thought about effects of changes in the board…

First, the interest rate on reserve balances (IORB), is set by a majority vote of the Board, not the FOMC. Historically, the Board has set IORB at an appropriate level to maintain the fed funds rate within the target range set by the FOMC. But, theoretically at least, a Board with a majority that did not agree with the FOMC decision could set IORB at a different – in this case lower – level. If the goal is to achieve lower rates, and the FOMC is not supportive, one unprecedented way to do that would be through this channel. That said, there may be limits to the related impact, as the FOMC sets the ONRRP rate and could continue to do so with a goal of keeping overnight repo rates near its target range. That would create unprecedented dynamics in money markets but potentially mute the impact of lower IORB out the curve.

and,

Second, in addition to approving new nominations for regional Fed bank presidents, every five years the presidents of the twelve regional banks come up for approval by the Board. This process is typically uncontentious and passes without notice, as the Board supports the leadership decisions of the regional Board of Directors of each bank. However, this need not continue to be the case. If the desire for lower rates met resistance from a more hawkish block of regional Fed presidents, a majority on the Board could take the unprecedented move of not approving some of the regional voters. Importantly, the next five-year approval is slated for Q1 next year.

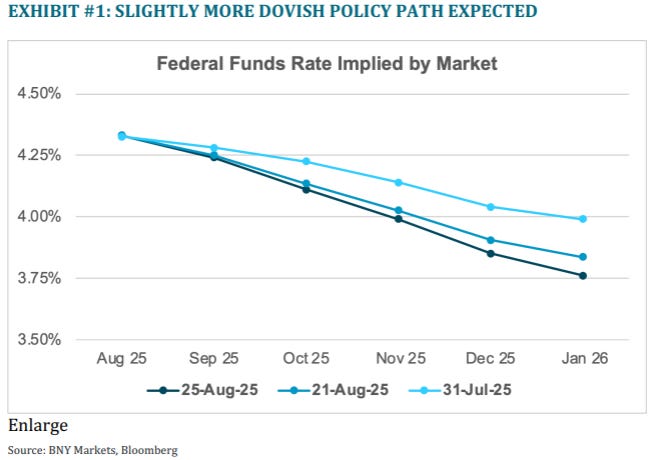

Does it risk ending an independent Fed? I strongly believe it is naive to think that it was ever politically independent, and it will just be a question of degree. The market has priced in interest rate cuts for a while, and as we saw earlier the track isn’t that different to before. If rates fall to zero immediately then there is an argument, but a Fed that cuts in line with last year’s forward track then it is tough to argue that much is different.

The “Powell spread” continues to fall, with a whole rate cut priced over the period Powell’s term finishes.

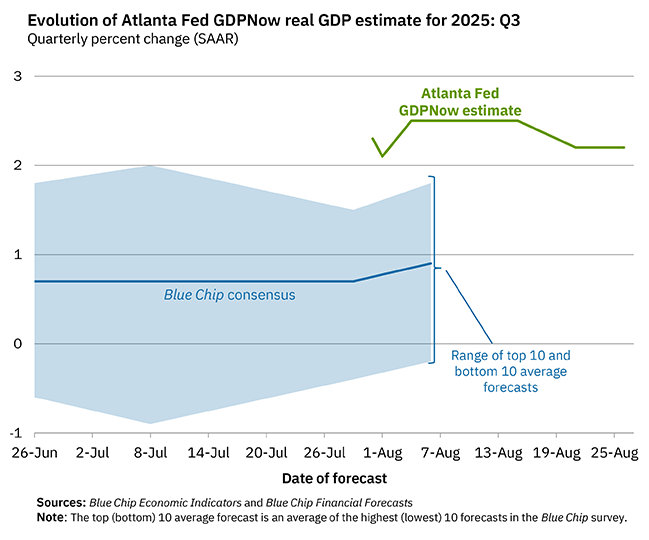

Moving back to the economy. Durable goods orders surprised to the upside this week, leading Goldman to update their Q3 tracking to 1.8% (but with final demand only at 0.6% indicating more give-back from trade is still coming).

The Atlanta Fed GDPNow model is showing >2% for Q3 growth.

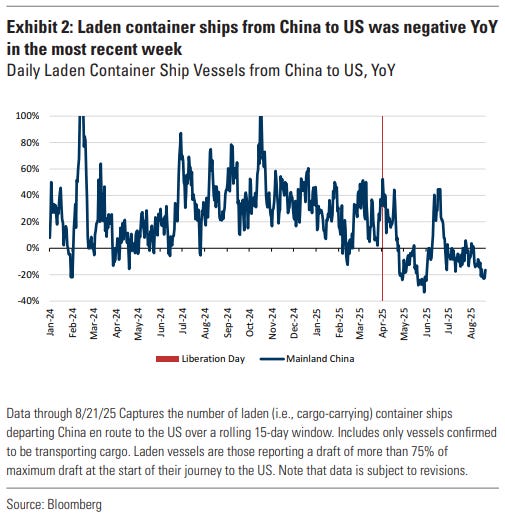

Trade is showing some moderation through container ship data. This all lines up with the debt dynamics suggesting that we are in a slower growth patch until tariff collection stops growing. Real GDP growth of 1-2% is consistent with this.

Chinese Involution

The Chinese rally against involution has caused ever falling 10y CGB rates to pick up more recently…

…along with onshore equities which have picked up quite a bit with much less fanfare than they did earlier this year.

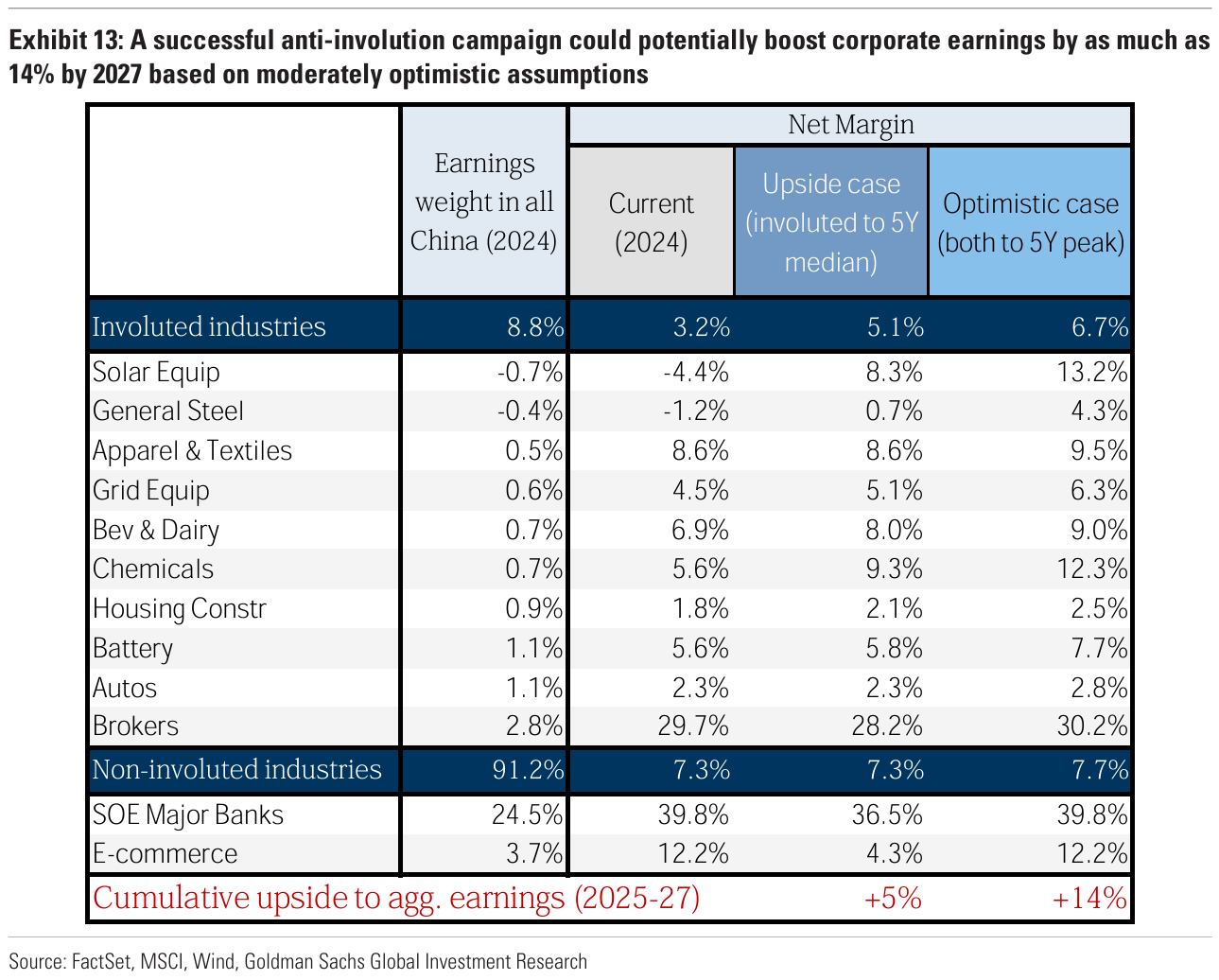

While more than a week old now, Goldmans did a good piece on the anti-involution drive, with their summary of the forecast earnings effect above.

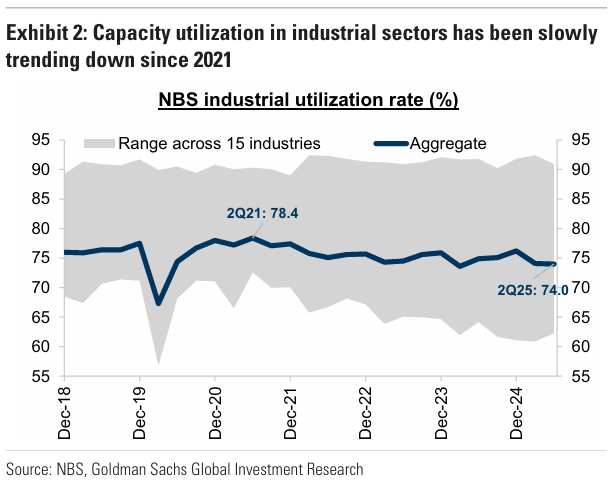

Deflation and profit stagnation has been caused by an increase in manufacturing investment with a decrease in prices. No surprises that capacity utilization has also fallen in that time.

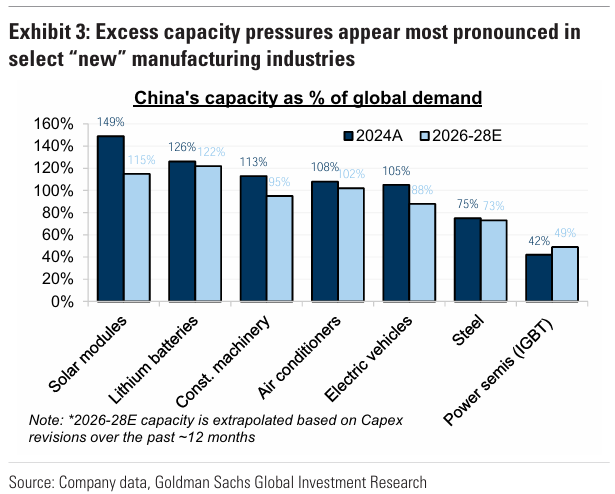

Supporting this assertion is that those select “new” industries that have received most capex are the most underutilised. The numbers in the chart above are mind-blowing. In solar, battery tech, construction machinery, air conditioners and EVs, China is greater than 100% of global demand. How could anyone possibly compete?

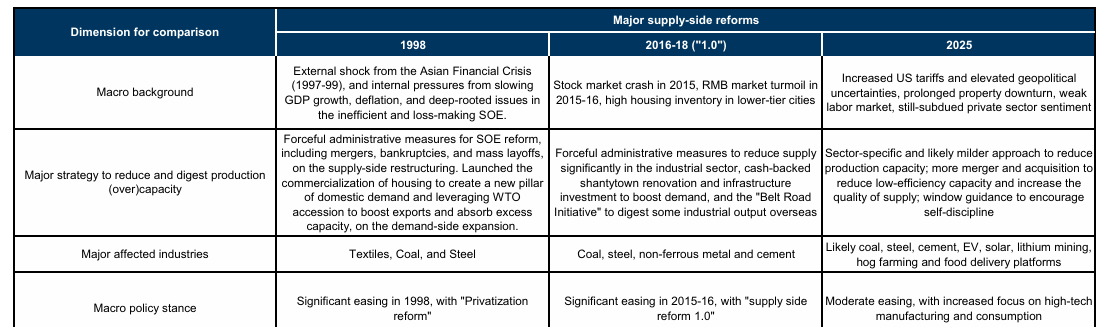

In the appendix, GS include a table on prior supply-side actions by Chinese leadership.

In both prior cases, the solution was really just to increase capacity utilisation by boosting investment elsewhere - in both cases it was property primarily, and then infrastructure second. These options aren’t available today.

This leaves the question on how it is going to be completed this time without defaults that we’ve seen in the property sector and the stagnation in activity that comes with that sort of unwind.

I’ve spoken of the Chinese EV industry repeatedly. It is by far the most visible industry that is experiencing the problem of “involution”, with many manufacturers supporting an industry of suppliers that have no choice but to accept extremely poor payment terms along with being squeezed on price.

In answer to this, CAAM (China Association of Automobile Manufacturers) has called on automakers to reject "bottom-line price wars" and compete via innovation in technology and services. In addition, 17 automakers have pledged supplier payment terms ≤60 days (it previously averaged 170 days).

Will this work to encourage the industry to increase pricing? I don’t see how it can. Breaking through into foreign markets requires the roughly 20% discount their cars are priced at to continue due to the lack of brand cache and dealer networks. Does anyone expect domestic buyers to make up for this loss, and for all of that to happen without anyone going bust?